- Miami’s fintech ecosystem gives founders unmatched access to Latin American capital flows and cross-border users.

- Compliance planning belongs in week one, not after the app is built, when rebuilding costs 40–60% of the original budget.

- The build-vs-buy decision at the architecture stage controls more of your budget than any other single choice you make.

- AI-native architecture costs 20–35% more upfront but saves 2–3x the cost of retrofitting AI features into a standard app.

- Florida’s MSB license takes 90–180 days; start the application during product discovery, never after development begins.

- Post-launch compliance runs 15–25% of the original development cost annually; budget for it before launch.

You have a fintech idea. You know it solves a real problem. But turning that idea into a working, compliant, market-ready app in Miami? That’s where most founders get stuck.

Miami now ranks among the top five US cities for fintech investment. And it sits at the center of Latin American capital flows, making it the only US city where you can consider banking app development for both domestic and cross-border markets at once.

But the ecosystem alone won’t build your app. You still need the right process, the right tech stack, and a compliance strategy that won’t blow up after launch.

That’s exactly what this guide covers.

Whether you’re a startup founder with a pitch deck and a deadline or a CTO at a financial services firm ready to go digital, we walk you through “how to build a fintech app in Miami”.

From app types and must-have features to costs, compliance, and choosing the right app developers in Miami, you’ll find all the answers here.

Let’s start with why Miami is the right city for fintech startup app development in Florida.

Why Miami Is the #1 City to Launch a Fintech App Right Now

Miami is the #1 US city to launch a fintech app because it offers unmatched access to Latin American markets, a dense fintech talent pool, and an investor ecosystem actively funding financial technology.

The numbers back that up.

Fintech Boom

Miami ranks among the top 10 fintech hubs in the world, according to Forbes.

The Miami Economic Development Council’s 2024 report states that since 2020, hundreds of new companies have entered the market. Brickell, Miami’s financial district, hosts regional headquarters for major banks, payment processors, and fintech startups. It earned the nickname “Wall Street South” for good reason.

In practice, this means: the infrastructure, the investors, and the talented fintech app developers are already in Miami. You build on top of an existing ecosystem that’s actively growing.

The LatAm Gateway Advantage

Miami processes more Latin American cross-border transactions than any other US city. Greater Miami Chamber of Commerce / Beacon Council, 2024 highlights that over 60% of Latin American multinational companies keep their US headquarters in Miami

Here is why that matters for your product.

If your fintech startup app development in Florida touches payments, remittances, lending, or investment, your users likely move money between the US and Latin America. Building in Miami means that reality shapes your architecture from day one.

Multi-currency support, cross-border compliance, and LatAm-specific payment rails become core features. Teams based here understand that instinctively.

Miami’s Talent and Investor Ecosystem

Since 2021, Miami has attracted thousands of tech founders, engineers, and venture capital firms.

According to Tracxn, the city hosts over 58 active tech accelerators and incubators. Major fintech-focused VCs have opened offices in Miami, drawn by Latin American deal flow and the city’s favorable tax environment.

For you, this creates a real advantage. Local developers who understand fintech compliance. Investors who know the LatAm market. A peer network of founders who’ve already navigated Florida’s regulatory landscape.

That combination exists here. It’s rare everywhere else.

Miami's Fintech Window Is Open, but the Ecosystem Is Filling Fast

We help you move before the market catches up and the early-mover advantage disappears. Launch with a fintech strategy built for compliance, scalability, and long-term growth.

Book Your Fintech Consultation Now →What Type of Fintech App Should You Build in Miami, FL?

Your fintech app type determines your compliance path, your tech stack, and your go-to-market strategy. In Miami, the highest-demand categories are payment tools, neobanks, and cross-border financial products, driven by the city’s position in the Latin American market.

Here’s a breakdown of every major fintech app type.

Payment Apps

These handle money transfers, bill splits, and digital wallets. In Miami, cross-border payment tools dominate. The city’s LatAm corridor generates billions in annual remittance volume, making payment apps one of the highest-demand categories in South Florida.

Neobanks

Fully digital banking with zero branches. A large immigrant and underbanked population (people with limited or no access to traditional banking services) creates strong demand for mobile-first banking app development in Miami that traditional institutions have historically underserved.

Lending Platforms

AI-driven loan origination and underwriting apps. Miami ranks among the top US cities for small business density, and many of those businesses actively seek faster, digital-first lending solutions outside traditional banks.

InsurTech Apps

These are digital-first insurance platforms. Miami’s property market is shaped by hurricane risk and rising premiums. Thus, it has produced one of the most active InsurTech user bases in the city.

Investment and Trading Apps

Platforms for stocks, ETFs, commodities, and crypto. Miami’s wealth management sector and its concentration of LatAm high-net-worth individuals make this a strong, growing category locally.

Personal Finance Apps

Budgeting, saving, and spending management tools. With nearly 47% of US adults rating their own financial literacy as average or below in the National Foundation for Credit Counseling’s 2024 Financial Literacy Survey, demand for accessible personal finance tools stays consistently high.

Crypto and Web3 Apps

Miami has positioned itself as a US crypto capital, hosting major Web3 events and attracting blockchain-focused startups and investors. However, blockchain app development in Miami often needs more than a standard tech stack. It requires a specialized architecture layer that most generalist teams can’t support.

How to Validate Your Fintech App Type Before Building

Here’s a pattern that repeats across failed fintech products: the team built first and validated later.

By the time users gave feedback, the architecture was locked, the budget was spent, and pivoting meant rebuilding from scratch.

Before you hire app developers in Miami, run the “20 user test.” Talk to 20 people who match your target user profile. Ask them: “If this app disappeared tomorrow, would you be upset?” Fewer than ten saying yes means the concept needs more work.

Must-Have Features for Fintech App in Miami

A successful fintech app needs three layers of features: core functionality users expect, AI-powered tools that drive retention, and compliance and security features that keep the product legal and trustworthy.

Features make or break a fintech app, and the list has grown significantly in the past three years. Users now expect more than a login screen and a transaction history. Investors expect AI readiness. Regulators expect compliance architecture baked in from the start.

Here’s exactly what fintech features your app needs across all three layers.

A) Core Features Every Fintech App Needs

These are the table-stakes features. Ship without them, and users leave on day one.

- Biometric Authentication: Fingerprint and face recognition login. Users expect this as the default passwords alone create friction and erode trust in financial products.

- Payment Gateway Integration: Stripe handles card payments globally. Plaid connects directly to US bank accounts. Zelle works for instant US bank transfers. Most Miami-built fintech apps use a combination of all three.

- Real-Time Transaction Dashboard: A visual, always-updated view of account activity. Users make faster, better financial decisions when they can see their data at a glance. Charts, spending breakdowns, and balance history all belong here.

- Push Notifications: Instant alerts for transactions, security events, and account changes. In Miami’s cross-border payment market, real-time notifications across time zones are a core user expectation.

- Multi-Currency Support: Essential for any Miami-built fintech app serving LatAm users. Your app should handle USD, BRL, MXN, COP, and other major LatAm currencies without requiring users to leave the app.

- In-App Customer Support: Live chat or AI-powered support built directly into the product. Users dealing with financial issues want answers fast; a support email address loses them permanently.

B) AI-Native Features That Investors Now Expect

Here’s a distinction that matters at the architecture level.

AI-native means your app is designed to run on machine learning models. AI-bolted means you built a standard app and added AI features in a later version.

The difference shows up in performance, cost, and investor perception. AI-native apps process data faster, personalize better, and scale. In fact, the fintech apps attracting investment in 2026 are built with AI at the core, not layered on after the fact.

These are the AI features Miami fintech investors are actively looking for right now.

- Fraud Detection and Prevention: Machine learning models that flag unusual transactions in real time. This runs in the background, so users never see it.

- AI-Powered Credit Scoring: Algorithms that assess creditworthiness using spending patterns, transaction history, and behavioral signals, beyond traditional credit bureau scores. Especially valuable in Miami’s LatAm market, where many users carry thin or foreign credit files.

- Personalized Financial Insights: The app analyzes user behavior and surfaces actionable recommendations. “You spent 40% more on dining this month” is useful. “Based on your pattern, you’ll run short before payday” is valuable.

- Robo-Advisory: Automated investment portfolio management based on user goals and risk tolerance. Removes the need for a human financial advisor, making wealth management accessible to users who previously couldn’t afford it.

- Conversational AI and Chatbots: Natural language interfaces that let users check balances, initiate transfers, and get support by typing or speaking naturally without navigating menus.

C) Compliance and Security Features

Security and compliance are architecture decisions. They shape how your entire app is built.

Treating them as features you add later is the most expensive mistake. Florida’s Money Services Business licensing requirements, federal KYC and AML obligations, and PCI DSS standards have direct implications for how your app handles, stores, and transmits financial data.

Here’s what your app must include.

- KYC — Know Your Customer: Identity verification at onboarding. Your app collects government ID, matches it against databases, and confirms the user is who they say they are. Required by US federal law for any app handling financial transactions.

- AML — Anti-Money Laundering Monitoring: Automated transaction monitoring that flags patterns consistent with money laundering. Required under the Bank Secrecy Act for US-registered financial apps.

- End-to-End Encryption: AES-256 encryption for stored data. TLS 1.3 for data in transit. These are the current industry standards. Anything below them creates regulatory and reputational risk.

- Two-Factor Authentication (2FA): A second verification step for logins and money movement. Standard practice across all regulated financial products in the US.

- PCI DSS Compliance: The Payment Card Industry Data Security Standard governs how your app handles card data. Building to PCI DSS from the start avoids costly audits and rebuilds later.

- Audit Trails: Every transaction, every state change, every user action logged with a timestamp. Regulators in Florida require the ability to produce complete transaction histories on request.

Teams in Miami often run into fintech compliance challenges that slow down launch. Most of them stem from treating security as a feature rather than a foundation.

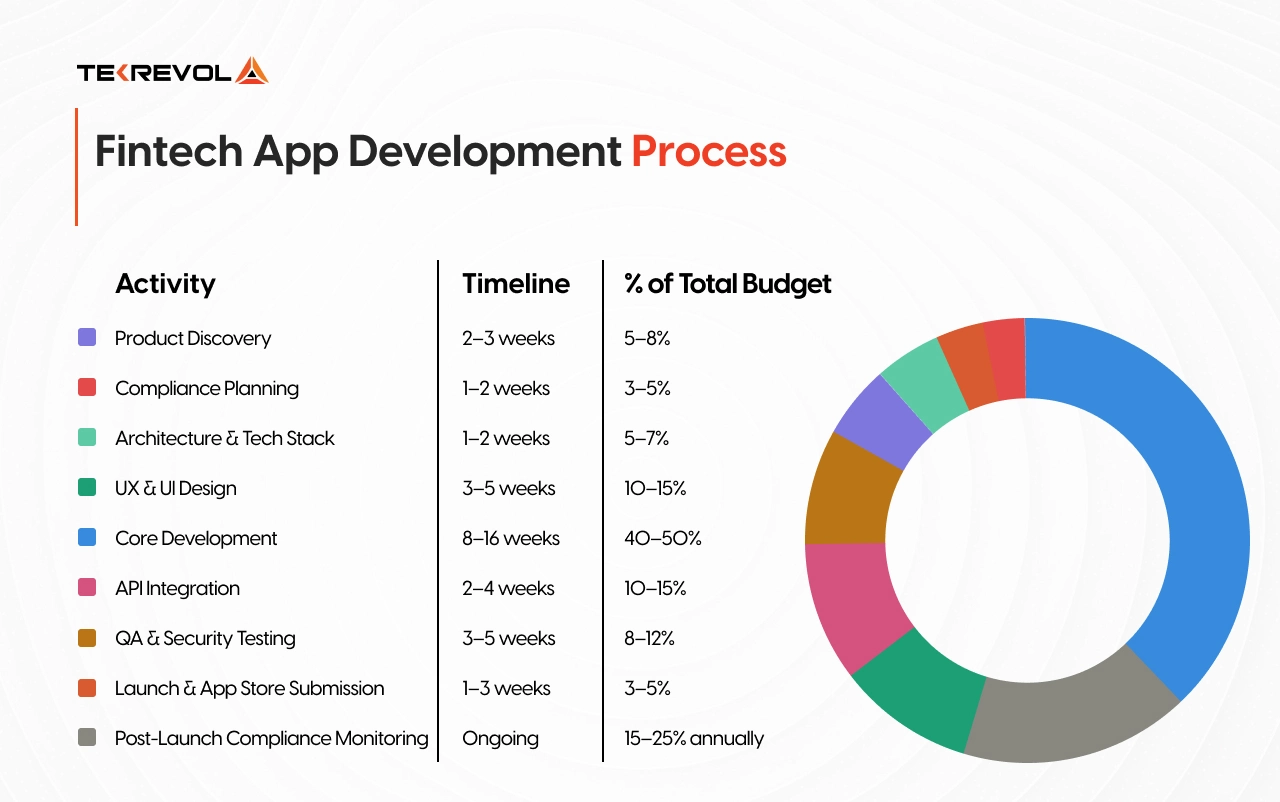

How to Build a Fintech App in Miami? Step-by-Step Workflow

Building a fintech app in Miami follows eight steps: discovery and compliance planning, architecture decisions, UX design, core development, API integration, QA and security testing, launch, and post-launch compliance monitoring.

Most fintech apps that fail do so in the first three steps, before a single line of code gets written.

Here’s the full roadmap built around one principle: compliance first, features second. Every step reflects what actually works for regulated fintech/banking app development in the Miami market.

Step 1: Product Discovery

Map your app’s core user flow, define your target audience, and identify the single problem your MVP solves. For Miami-based fintech apps, this phase includes a LatAm market assessment: who your cross-border users are, what currencies they use, and what payment rails they rely on.

Deliverables: user personas, core user flow diagram, feature priority list, and a preliminary tech stack recommendation.

Step 2: Compliance Planning

This step separates teams that launch on time from teams that rebuild in year two.

Before architecture decisions get made, map every regulatory requirement your app triggers. In Florida, this means:

- MSB License — required for any app transmitting money in Florida

- FinCEN Registration — a federal requirement for money services businesses

- KYC/AML Architecture — how your app verifies users and monitors transactions

- PCI DSS Scope — which parts of your app touch card data, and how

Different app types carry different obligations. A payment app, a lending platform, and a crypto wallet each trigger a different compliance stack in Florida.

Step 3: Architecture and Tech Stack Decisions

Your architecture determines your scalability, your security posture, and your long-term maintenance costs. Two decisions dominate this phase.

Native vs Cross-Platform

Native iOS and Android apps offer stronger security controls and better access to device hardware, both of which matter in fintech. Cross-platform frameworks like React Native reduce build time and cost, with a small performance trade-off.

For most Miami fintech MVPs, React Native development delivers the right balance.

Build vs Buy: The API Decision Matrix:

| Function | Recommendation | Tool |

| Bank account access | Buy | Plaid |

| Payment processing | Buy | Stripe |

| User authentication | Buy | Firebase |

| Credit score access | Buy | Experian API |

| KYC verification | Buy | Jumio / Onfido |

| Core business logic | Build | Custom |

| Compliance reporting | Buy | Unit21 / Flagright |

| Data visualization | Buy | D3.js |

Building what these APIs already do costs months and adds risk. Custom development belongs only where your product is genuinely differentiated.

Step 4: UX and UI Design

Fintech design operates under a different set of rules than other app categories.

Users make decisions about their money on every screen. The design has to communicate one thing above everything else: your money is safe here.

That means:

- Zero ambiguity in transaction flows: users always know what action they’re taking

- Instant visual confirmation for every money movement

- Clear, plain-language error states: never a generic “something went wrong” message

- Accessible typography and contrast ratios for users across age groups and devices

For Miami’s multilingual user base, design should support both English and Spanish interfaces from the start. Adding language support post-launch requires a full redesign.

Step 5: Core Development

Development follows the compliance architecture and design system established in Steps 1–4. Work in two-week sprints with clear acceptance criteria for every feature.

For Miami fintech apps, development priorities run in this order:

- User authentication and onboarding with KYC verification

- Core financial transaction flow

- Real-time dashboard and transaction history

- Notification system

- Multi-currency support for LatAm users

- AI features such as fraud detection, personalization, and credit scoring

Build your compliance pipeline to cover audit trails, transaction logging, and data encryption in the first sprint. Everything else builds on top of it.

Step 6: API Integration

Integrate your third-party APIs in parallel with core development: Plaid for bank connectivity, Stripe for payments, Firebase for authentication, and your chosen KYC provider.

Each integration requires building fault-tolerant error handling around it. Your app needs to handle every failure state gracefully, especially during money movement.

Step 7: QA, Security Testing, and Launch

Fintech QA goes beyond standard app testing. Three additional layers apply.

- Security Penetration Testing: A third-party security team actively attempts to breach your app before launch. Required for any app handling financial data, and increasingly expected by enterprise clients and investors.

- Load Testing for Payment Flows: Simulate 100+ concurrent users initiating transactions simultaneously. Payment infrastructure that works for 10 users can fail at 1,000. Miami’s fintech apps serving high-volume LatAm remittance users need to validate this before launch.

- Compliance Audit: A formal review of your KYC flow, AML monitoring, data encryption, and audit trail completeness before submission to app stores and regulators.

App store submission adds 1–3 weeks for fintech apps. Apple and Google apply additional review scrutiny to financial products.

Step 8: Post-Launch Compliance Monitoring

Launch is not the finish line; it is the start of your ongoing compliance obligations.

Post-launch, your team actively manages:

- Ongoing KYC monitoring: re-verifying users whose circumstances change

- AML transaction monitoring: flagging and reporting suspicious activity to FinCEN

- Regulatory reporting: quarterly and annual filings with Florida’s Office of Financial Regulation

- Security patching: applying updates to encryption libraries, authentication systems, and third-party APIs

- Performance monitoring: tracking API uptime, transaction success rates, and error rates across payment flows

A closer look at how fintech apps get built from the ground up shows why post-launch planning belongs in your pre-launch budget. Founders who treat it as an afterthought face the most expensive surprises.

How Much Does Fintech App Development Cost in Miami?

Fintech app development in Miami costs between $40,000 for a simple MVP and $400,000+ for a full-scale platform. The final number depends on your app type, compliance scope, AI features, and whether you build custom infrastructure or use proven APIs.

Cost is the question every founder asks first. This section gives you real numbers, broken down by app type, development phase, and the factors that push costs up or down.

Cost by Fintech App Type

Miami fintech development costs reflect both the complexity of the product and the compliance scope it triggers. A personal finance app and a neobank share some features but carry completely different regulatory and architecture costs.

| App Type | MVP Cost | Full Build | Timeline |

| Personal Finance App | $30,000–$60,000 | $80,000–$150,000 | 3–5 months |

| Payment / Wallet App | $40,000–$70,000 | $100,000–$180,000 | 3–5 months |

| Lending Platform | $60,000–$100,000 | $150,000–$280,000 | 4–7 months |

| Neobank / Banking App | $80,000–$120,000 | $200,000–$350,000 | 5–8 months |

| Investment / Trading App | $70,000–$130,000 | $200,000–$400,000 | 5–9 months |

| Crypto / Web3 App | $60,000–$110,000 | $180,000–$380,000 | 4–8 months |

Ranges reflect typical Miami market rates for full-cycle development, including design, development, QA, and launch.

Miami development rates run higher than offshore alternatives, typically $100–$180 per hour for senior fintech developers locally. The trade-off is proximity, timezone alignment, and a local team that understands Florida’s regulatory environment.

What Drives Fintech Development Costs Up

Understanding cost drivers gives you real control over your budget.

Compliance Scope

Compliance and security features typically consume 15–40% of the total development budget, depending on app type. A crypto wallet development with VASP licensing requirements costs significantly more than a personal finance app. Map your compliance scope in discovery; it directly sets your budget floor.

AI Features

AI-native fintech apps cost 20–35% more to build than standard apps. Fraud detection models, credit scoring algorithms, and personalization engines require specialized ML engineering, additional data infrastructure, and more extensive testing cycles.

Custom Infrastructure vs API-First

Teams that build custom payment processing, authentication, or KYC systems spend 60–70% of their budget on features that proven APIs handle better. Every dollar spent rebuilding Stripe is a dollar taken away from your core product.

Cross-Border Architecture

Miami fintech apps serving LatAm users need multi-currency support, cross-border payment rails, and OFAC screening built in from the start. Adding these features post-launch costs 3–4x more than building them in the initial architecture.

Native vs Cross-Platform Development

Native iOS and Android development costs 30–40% more than cross-platform frameworks. For most Miami fintech MVPs, cross-platform delivers the right balance of cost, performance, and security.

Hidden Costs Most Miami Founders Miss

The fintech app development cost estimate covers building the app. These are the costs that appear after launch and that most fintech founders only discover after the first invoice arrives.

Third-Party API Fees

Plaid charges per API call. Stripe takes a percentage of every transaction. KYC verification providers charge per user verified. At low volume, these costs feel minor, but at scale, they become a significant operational line item.

Compliance Operations

Ongoing AML monitoring, quarterly regulatory reporting, and Florida OFR license renewals run $3,000–$8,000 per month for a typical Miami MSB. Budget for this before launch.

Security Audits

Annual penetration testing and PCI DSS compliance audits cost $15,000–$50,000, depending on scope. Enterprise clients and institutional partners in Miami require current audit reports before signing agreements.

Cloud Infrastructure Scaling

Your AWS or Azure bill at 1,000 users and your bill at 100,000 users share nothing in common. Cloud costs grow non-linearly with transaction volume. Fintech apps that process payments at scale need cloud infrastructure management modeling before launch.

App Store Updates and Maintenance

OS updates, API version changes, and security patches require ongoing development work. Budget 15–25% of the original development cost annually for maintenance.

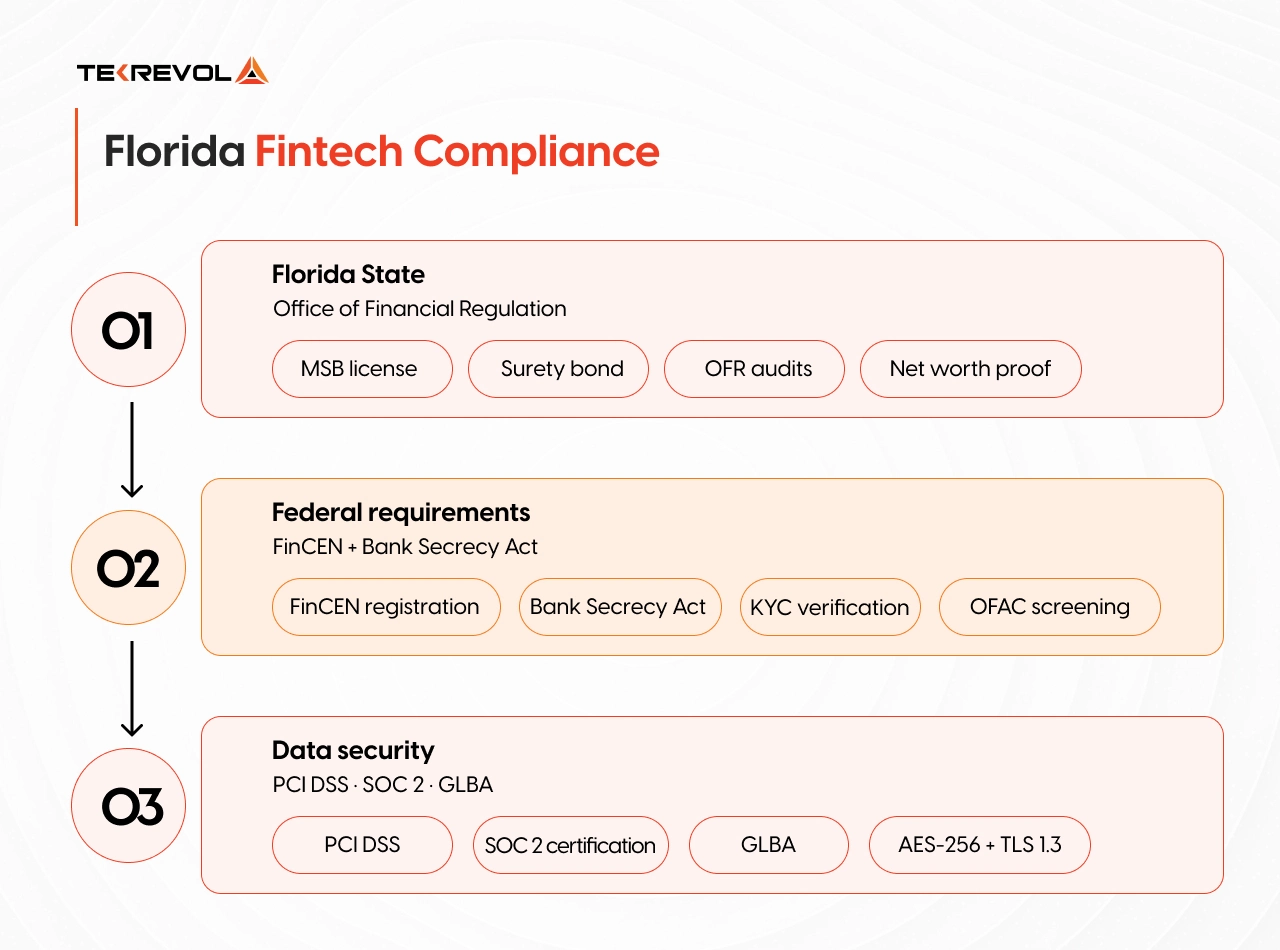

Florida Fintech Compliance: What You Must Know Before You Build

Florida fintech apps must comply with state MSB licensing, federal FinCEN registration, KYC/AML requirements, and data security standards, including PCI DSS and SOC 2. Getting this wrong before launch costs more to fix than it does to build correctly from the start.

State Licensing Requirements

Florida regulates money services businesses through the Office of Financial Regulation (OFR). If your app transmits money, exchanges currency, cashes checks, or issues payment instruments, you need a Florida Money Services Business (MSB) license before you go live.

Here’s what the licensing process involves:

- Background checks on all principals and owners

- A surety bond, typically between $10,000 and $2 million, depending on transaction volume

- A detailed business plan and financial statements

- A compliance program document covering AML policies and procedures

- Proof of net worth requirements set by the OFR

⏱ Timeline: Florida MSB license applications take 90–180 days to process. Factor this into your launch timeline before your first development sprint starts.

Action tip: Start your Florida OFR application in parallel with your product discovery phase. A licensing attorney familiar with Florida fintech regulations saves significant time and reduces the risk of application rejection.

Federal Compliance Requirements

Every US fintech app that handles financial transactions operates under federal law. Here’s what applies directly to Miami-built products.

FinCEN Registration: The Financial Crimes Enforcement Network requires all US money services businesses to register federally within 180 days of starting operations. Registration is free but mandatory; operating without it carries criminal penalties.

Bank Secrecy Act (BSA): Requires fintech apps to maintain records of financial transactions and report suspicious activity. Your app’s AML monitoring system must be built to BSA standards from day one.

KYC Requirements: Federal law requires financial apps to verify the identity of every user before allowing money movement. At a minimum, your KYC flow collects full legal name, date of birth, address, and a government-issued ID number.

AML Program Requirements: Your app must maintain a written AML compliance program covering “internal policies, a designated compliance officer, ongoing employee training, and independent auditing.”

For Miami-built apps serving LatAm users, cross-border transactions add OFAC screening requirements; your app must check every transaction against the Office of Foreign Assets Control sanctions list.

Data Security Standards

Regulatory compliance covers how your app handles money. Data security standards cover how it handles information.

For Miami fintech apps, three standards apply most directly.

PCI DSS — Payment Card Industry Data Security Standard

Governs how your app collects, stores, and transmits card data. Any app that touches card numbers, even briefly, falls under PCI DSS scope.

PCI DSS compliance involves 12 core requirements covering network security, access controls, encryption, monitoring, and regular security testing. Building to these standards from the start costs a fraction of what a post-breach remediation costs.

SOC 2 — Service Organization Control 2

A voluntary but increasingly expected security certification for fintech apps handling sensitive user data. Enterprise clients, institutional investors, and banking partners in Miami regularly require SOC 2 compliance before signing agreements.

SOC 2 audits evaluate five trust principles: security, availability, processing integrity, confidentiality, and privacy.

GLBA — Gramm-Leach-Bliley Act

Federal law requires financial institutions to explain their data-sharing practices and protect sensitive user data. Applies to any app collecting personal financial information from US consumers.

Key GLBA requirements for fintech apps:

- A written information security program

- A privacy notice delivered to users at onboarding

- Limits on sharing personal financial data with third parties

The Cost of Getting Compliance Wrong

- The average cost of a data breach in the financial services sector reached “$6.08 million” as per the IBM Cost of a Data Breach Report 2024.

- Florida’s OFR actively enforces MSB license requirements, with documented enforcement actions including fines and license revocations (Florida OFR Enforcement Actions Register, 2024).

- A compliance rebuild mid-development, when architecture is partially locked, costs 40–60% of the original development budget.

Those numbers make the case on their own. Compliance built in from the start costs a fraction of compliance bolted on after the fact.

Miami’s fintech market rewards teams that treat regulatory requirements as a product feature. Reason? Users, investors, and banking partners all evaluate your compliance posture before they commit.

How to Control Your Fintech App Development Budget

Costs go up when the scope expands without control. Here’s how Miami’s most successful fintech teams keep budgets on track.

Start with an MVP, Validate, Then Expand

An MVP scoped to one core user flow account opening and a first transaction, for example, costs a fraction of a full product. Validate it with real users before adding features. Every feature you add post-validation has evidence behind it. Every feature you add before validation is a bet.

Prototype Before You Build

An interactive prototype costs $5,000–$15,000 and takes 2–4 weeks. It lets real users interact with your core flow before a single line of production code gets written. Features that confuse users in a prototype get fixed cheaply. Features that confuse users in a live app cost significantly more to rework.

Buy Commodity, Build Differentiation

Use the API decision matrix from Step 3. Every hour your team spends building authentication, payment processing, or KYC verification is an hour taken away from the features that make your product worth choosing.

Fix Your Compliance Architecture Early

A compliance rebuild mid-development costs 40–60% of the original development budget. Getting your MSB license application, KYC architecture, and AML program right in weeks one and two costs a fraction of fixing them in week sixteen.

Why Choose TekRevol for Fintech App Development in Miami?

TekRevol is a full-stack fintech app development company with a physical office in Brickell. Our deep compliance expertise and a proven track record of shipping regulated financial products for startups and enterprises across the US and Latin America separate us as specialists.

Local Presence

TekRevol’s Miami office sits at 400 NW 26th St, inside the city’s tech corridor, minutes from Brickell’s financial district.

That means face-to-face collaboration when your product needs it. Our app developers in Miami operate in your timezone, understand Florida’s regulatory environment firsthand, and have built fintech products for the same LatAm cross-border market your users belong to.

Full-Stack Fintech Specialization

TekRevol covers every phase of fintech development: product discovery, compliance architecture, UX design, core development, API integration, QA, launch, and post-launch monitoring.

That matters because fintech products break when handoffs happen between specialists who work in isolation. A compliance consultant who never talks to your backend team produces requirements that the architecture can’t support.

The technology stack covers iOS, Android, React Native, Node.js, Python, Firebase, and the full suite of fintech APIs, Plaid, Stripe, Jumio, Unit21, and beyond.

Proven Track Record

TekRevol has shipped fintech products across payments, lending, investment, and crypto for startups building their first MVP and enterprises modernizing legacy financial infrastructure. Recent fintech builds include:

Revcoin, a blockchain-based crypto equity platform that gives employees transparent ownership stakes through ERC-20 tokens on the Ethereum network. Smart contracts handle fund management and reward distribution automatically, removing the need for manual administration.

Recognition from INC. 5000 as one of America’s fastest-growing companies and a 4.8 rating across 83+ Clutch reviews reflects a consistent track record across markets, app types, and development budgets.

Compliance and Security Expertise

Florida’s MSB licensing requirements, federal KYC and AML obligations, PCI DSS, SOC 2, and GLBA compliance are built into TekRevol’s development process.

Every fintech engagement starts with a compliance mapping session. Every product ships with audit trails, end-to-end encryption, and a documented AML program in place.

You now have the full picture of the process, the compliance requirements, and the cost breakdown for building a fintech app in Miami’s market.

Ready to Launch a Fintech App in Miami?

Book a conversation with TekRevol and get a detailed scope, timeline, and compliance-first development plan tailored to your app type, budget, and regulatory requirements.

Start Your Project Today →