- BNPL app development requires a lending engine, compliance layer, and payment rails; all built in sync.

- A production-ready BNPL MVP costs $30,000–$80,000 and takes 3–5 months with the right development partner.

- BNPL has consumer, merchant, and admin panels. Each serves a distinct purpose, so weakness in one breaks the full platform.

- Healthcare, travel, and B2B BNPL are the fastest-growing verticals with the least competition from generalist providers.

- Compliance built at Step 1 costs a fraction of compliance retrofitted after your first regulatory audit.

- The recommended BNPL tech stack pairs React Native or Flutter (frontend) with Node.js or Python (backend), with Redis for sub-500ms credit decisioning at checkout.

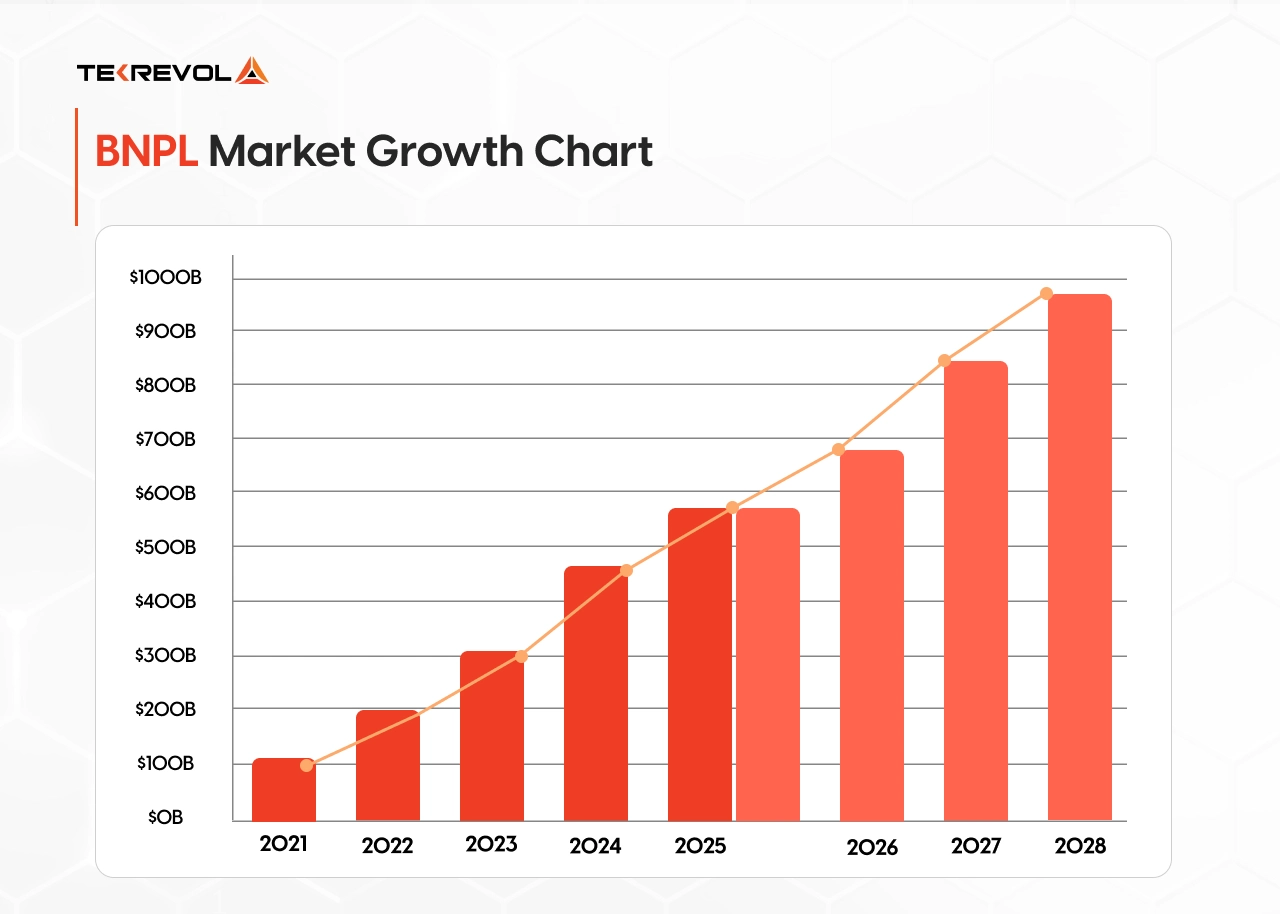

Online shopping has made Buy Now Pay Later (BNPL) one of the fastest-growing payment methods. According to Juniper Research, global BNPL transaction volume hit $560 billion in 2025. That’s a 13.7% year-on-year increase, and the number keeps climbing.

That is why founders, product teams, and enterprises are moving to build BNPL platforms. But BNPL app development takes more than a payment integration. You’re combining lending, compliance, and real-time risk assessment into one experience. Miss the compliance, and you’ll face a regulatory problem. Working with an experienced fintech app development company keeps you from costly rebuilds later.

We walk you through how to build a BNPL platform. This guide covers the features, architecture decisions, real cost ranges, and the compliance requirements most teams learn about too late. Whether you’re a startup founder scoping your MVP or a CTO evaluating a development partner, this is your end-to-end playbook.

What Is BNPL? [Quick Overview]

Buy Now, Pay Later (BNPL) is a short-term financing model. It lets shoppers pay for a purchase in fixed installments rather than all at once. The shopper pays nothing upfront beyond the first installment. The platform carries the credit risk until the balance clears.

Most plans are interest-free, with payments on a fixed weekly or bi-weekly schedule. The merchant gets paid upfront; the BNPL provider carries the credit risk.

What Makes BNPL Different From a Payment Gateway

A payment gateway moves money, whereas BNPL extends credit. Those are two different problems and two very different systems to build.

When a shopper uses Stripe or PayPal, the transaction clears instantly. The merchant receives payment, and the customer pays from their account.

BNPL works differently. The BNPL provider pays the merchant upfront. The customer repays the provider over time in fixed installments. That means you’re building a lending product, a payment product, and a risk management system all in one platform.

| Feature | BNPL | Credit Card | Payment Gateway |

| Who pays the merchant upfront | BNPL provider | Card network/bank | Customer directly |

| Interest for consumer | None (short-term) | Yes, revolving rate | N/A |

| Credit check required | Soft check/alt data | Hard credit inquiry | None |

| Risk bearer | BNPL provider | Issuing bank | None (pass-through) |

| Revenue model | Merchant fees + late fees | Interest + annual fees | Transaction % fee |

| Regulatory category | Consumer credit (varies by market) | Consumer credit | Payment service |

The 3 BNPL Models You Can Build

- Pay-in-4: Four equal payments over six weeks. First payment due at checkout. Typically interest-free. This is the Klarna and Afterpay model and the most common starting point for new platforms.

- Pay-in-30: It defers the full payment by 30 days. This model is common in B2C e-commerce where checkout friction matters more than interest income.

- Long-term installments stretch repayments across 3 to 24 months. Interest usually applies after an introductory period.

Each model carries a different compliance profile, risk, and revenue structure. Your choice here shapes your entire embedded finance app development scope, so lock this in before you build anything.

BNPL Market Size, Growth & Opportunity in 2026

The global BNPL market processed $560 billion in gross merchandise value in 2025. It serves over 380 million users across 50+ countries.

According to Yahoo Finance, 91.5 million US consumers used BNPL last year, up from 86.5 million the year before. That number is projected to reach 96.3 million in 2026.

- Over 380 million people used BNPL globally in 2024. Analysts project it will reach 670 million by 2028 as emerging markets accelerate adoption. (Source: Chargeflow)

- BNPL provider revenue is forecast to reach $196 billion by 2032, growing at a compound annual rate of 23.8%. (Source: Persistence Market Research)

- Online channels will account for 84.7% of all BNPL transactions in 2026, reflecting the global shift to mobile-first shopping. (Source: Fortune Business Insights)

Three forces are driving that growth across every major region.

Shopper’s Credit Aversion

Over 62% of shoppers prefer flexible payment options over credit cards (Global Growth Insights). BNPL fits that preference. It spreads costs without accumulating revolving debt.

Merchant Conversion Lift

Merchants that offer BNPL at checkout see up to 85% higher average order values. Cart abandonment rates drop by up to 34%. (Capital One Shopping, 2026)

Vertical Expansion Beyond Retail

BNPL is moving into healthcare, travel, education, and B2B procurement. Each vertical carries lower competition than standard retail BNPL and a growing addressable market.

First-Mover Advantage in BNPL Is Still Available

Share your idea with TekRevol, and we’ll break down exactly what it takes to launch quickly, stay compliant, and compete before the market becomes saturated.

Get Your Free Plan →How to Build a BNPL App: Step-by-Step Process

Building a BNPL platform follows the same flow, covering UI/UX design, QA, soft launch, and post-launch monitoring.

What separates it from a standard fintech app development process is a credit decisioning layer, a compliance architecture, and a risk management system that a payment app never needs.

The full BNPL app development takes 4 to 12 months. Product complexity, team size, and the number of target markets drive that range.

1) Map your regulatory requirements

Start with regulatory mapping. BNPL is classified as a lending product in most jurisdictions. That classification changes your entire compliance burden. For the US, that means CFPB oversight, a lending license in each state you plan to operate in, and full Truth in Lending Act disclosure at every customer touchpoint.

The MVP Trap

A BNPL MVP launched without compliance becomes a liability. Regulatory debt accumulated post-launch can halt operations, trigger fines, and force expensive re-architecture. Build compliance from Step 1. It is the only way to scale across markets.

2) Choose your BNPL model and revenue streams

Your choice of model shapes the entire technical build, so lock this in early. Pay-in-4 is the simplest to build and the most consumer-familiar. B2B BNPL targets a different buyer entirely and demands a separate merchant onboarding and invoicing infrastructure.

On the revenue side, define your merchant discount rates, typically 2 to 8 percent. Factor in late fees and any interest that applies to longer-term plans.

3) Design your UI/UX flows

BNPL’s biggest UX challenge is earning user trust at the point of checkout. A shopper decides whether to use BNPL in under 10 seconds. Friction at that moment loses the sale. Wireframe your four core flows before development starts:

- onboarding and KYC,

- the checkout credit decision screen,

- the installment schedule display, and

- the repayment dashboard

The repayment dashboard is the most underinvested screen in most BNPL apps. Yet it directly affects late payment rates and user retention.

4) Build the credit engine and payment rails

This is the most technically demanding phase of the build. Your credit engine processes applications and queries bureau data. Alongside the credit engine, build your payment rails: transaction processing, installment tracking, and automated merchant settlement. The quality of fintech software development company at this stage directly determines your approval speed, default rates, and compliance exposure at scale.

5) Integrate merchant tools

At minimum, your platform needs live connections to a credit bureau, a payment gateway, a KYC provider, and at least one e-commerce platform. Go with Experian or TransUnion for credit; Stripe or Adyen for payments; Jumio or Onfido for identity, and Shopify or WooCommerce for merchant reach.

Run every API in a sandbox environment before it touches production. One misconfigured credit reporting integration can trigger CFPB penalties, so test thoroughly.

6) Run compliance audit

Security hardening comes before any external testing.

- TLS 1.3 covers data in transit

- AES-256 covers data at rest

- OAuth 2.0 manages authentication

- PCI-DSS covers your obligations on payment card data

Run a compliance audit against each target market before the first external user touches the product.

On the compliance side, run a full audit against every jurisdiction you plan to launch in. Engage a third-party compliance specialist for each market.

Gaps found at this stage cost a fraction of what they cost after launch.

7) QA, UAT, and soft launch

BNPL flows involve money, which means edge cases in testing carry real consequences.

Test every flow end-to-end: onboarding, credit decisions, checkout, repayments, failed payments, and refunds. Each one involves real money. Edge cases here carry real consequences.

Once QA clears, run UAT with a small group of real users and live merchants. What they catch in two weeks saves months of post-launch fixes. Collect structured feedback on friction points, decision screen clarity, and repayment flow usability.

8) Full Launch and Continuous Iteration

Deploy to app stores and production infrastructure. Monitor default rates, fraud signals, conversion metrics, and merchant settlement performance in real time.

Use live performance data to decide what comes next: new verticals, new merchant segments, or new features like virtual cards and longer-term plans. Let the repayment data drive the roadmap. It tells you more than any product brief will.

BNPL App Development Cost and Timeline

BNPL development costs sit between $30,000 and $300,000. The range is wide because the product scope varies just as much.

An MVP for a single market costs $30,000 to $80,000 and takes 3 to 5 months. A full-scale enterprise platform with multi-market compliance, AI credit scoring, and a merchant portal runs $150,000 to $300,000 and takes 8 to 12 months.

The embedded finance app development costs vary widely depending on what you are building and where. The table below breaks it down by tier.

| Tier | Cost range | Timeline | Best For |

| MVP | $30,000 – $80,000 | 3–5 months | Startups validating demand |

| Mid-tier | $80,000 – $150,000 | 5–8 months | Funded startups or vertical BNPL |

| Full-scale | $150,000 – $300,000+ | 8–12 months | Scaling platforms or enterprise deployments |

Five factors affect BNPL development budgets

- Team location. Offshore teams in South Asia or Eastern Europe typically cost 40 to 60 percent less per hour than onshore equivalents. Quality depends on the partner, not the geography.

- Number of BNPL models. A Pay-in-4 only product costs less to build. Adding Pay-in-30 and long-term installments increases both development time and compliance requirements.

- Compliance scope. Single-market compliance is manageable. Building for multiple jurisdictions simultaneously can double engineering hours.

- Credit scoring model. Rule-based scoring is faster and cheaper to build. Switching from rule-based to ML credit scoring adds 4 to 8 weeks to the build. It is worth it, but only once you have enough repayment data to train the model.

- Third-party integrations. Every additional third-party integration adds 1 to 3 weeks. Each one needs build time, testing time, and a sandbox run before it goes near production.

Core Features of a BNPL App You Need to Build

A BNPL platform has three distinct user layers: the consumer panel, the merchant panel, and the admin panel. Each panel serves a distinct purpose and has its own necessary fintech features requirements. All three must work in sync for the platform to function.

Here’s what goes into each one.

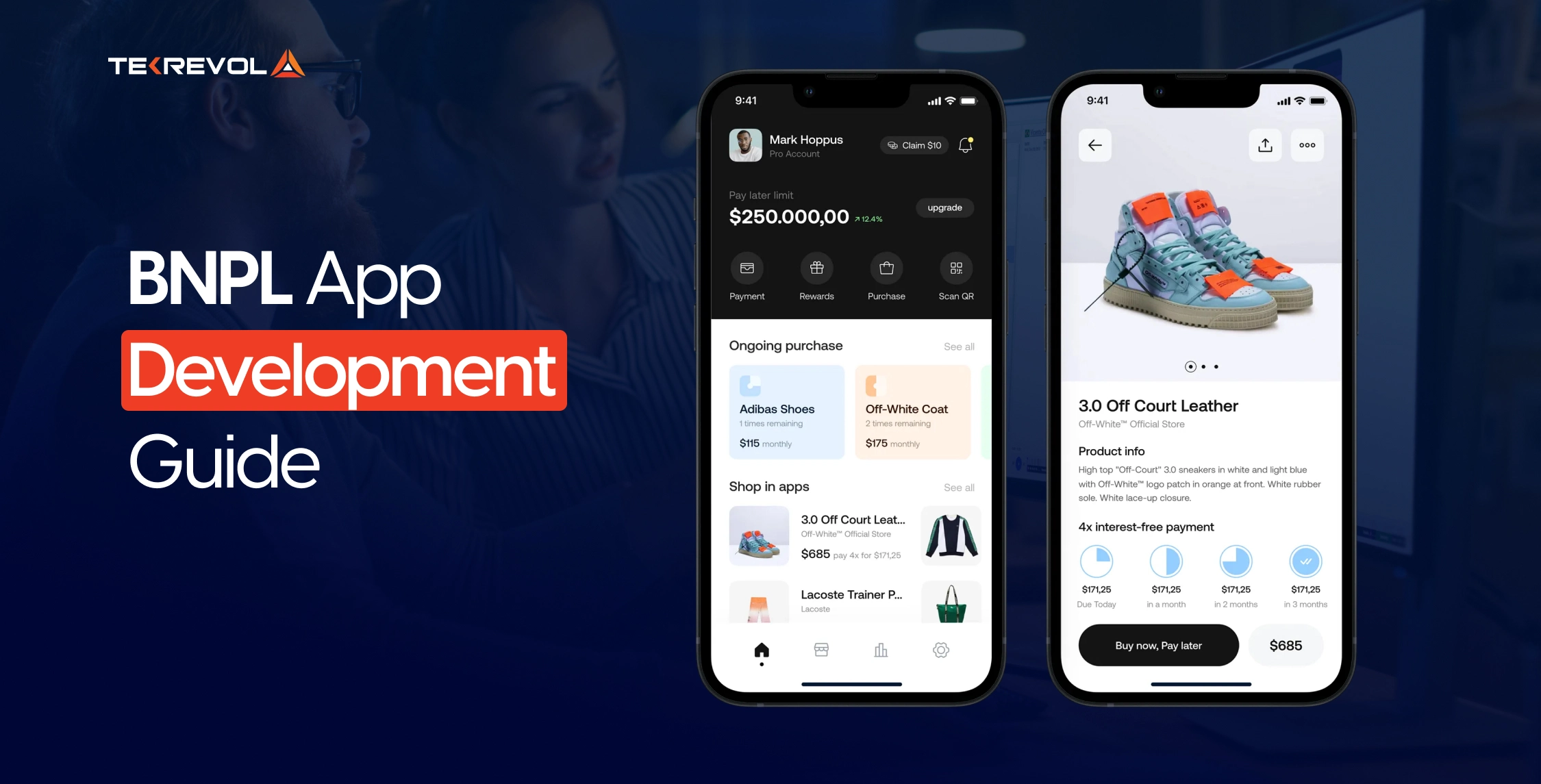

Consumer-Facing Features: Shopper panel

These are the features your end users interact with directly. Each one either builds or breaks the shopper’s confidence in your platform.

- KYC and onboarding: Verify identity at signup using document upload and a liveness check. A soft credit pull at this stage keeps friction low without affecting the shopper’s credit score.

- Instant credit decisioning: The shopper gets a yes or no in under two seconds. Anything slower loses the sale.

- Virtual card generation: Let users pay at any Visa or Mastercard terminal, even where no merchant-side BNPL integration exists.

- Installment scheduler: Shows the full repayment timeline before the shopper confirms the purchase. Seeing the plan up front cuts disputes later.

- Repayment dashboard: One screen for all active plans, upcoming payments, and payment history. Shoppers who can track what they owe pay on time more often.

- Push notifications: Automated reminders before each due date. A well-timed push notification does more for default rates than most credit scoring improvements.

- In-app dispute resolution: Shoppers raise payment or refund issues inside the app. Keeping them there shortens resolution time and reduces churn.

B) Merchant-Facing Features: Merchant panel

Your BNPL platform only generates revenue when merchants accept it. How fast they integrate determines how fast you grow.

- API and SDK: A developer should be able to integrate your SDK in a single afternoon. Support for Shopify, WooCommerce, and Magento covers the majority of your early merchant targets.

- POS compatibility: QR code and virtual card flows bring BNPL into physical retail without extra hardware. In-store adoption opens a transaction channel most BNPL-first competitors overlook.

- Analytics dashboard: Merchants want to see the conversion lift BNPL drives for their store. Surface order volume, average order value changes, and category-level data in one view.

- Settlement management: Automated daily or weekly settlement with clear reconciliation reporting. Merchants who trust the payout process stay on the platform.

- Refund and chargeback handling: A merchant-initiated refund updates the shopper’s installment schedule. Manual correction at this stage is a support ticket waiting to happen.

- Merchant onboarding portal: Self-serve registration, KYB verification, and API key management. Every merchant your team does not need to onboard is a merchant you acquire at zero marginal cost.

C) Admin Panel Features: Operations panel

Your operations team runs the platform from here. Risk, compliance, and configuration all live in the admin layer.

- Credit risk engine: Sets and adjusts credit limits per user based on real-time scoring data and repayment behavior.

- Interest & fee configuration: Controls APR, late fees, and promotional interest-free periods configurable per merchant segment or geography.

- Fraud monitoring dashboard: Real-time alerts on suspicious transaction patterns. Integrates with device fingerprinting and behavioral analytics.

- User management: Full customer record access, manual credit limit overrides, and account suspension, all from one screen.

- Regulatory reporting: Automated compliance reports for financial regulators across the US, UK, MENA, and Asia-Pacific.

- Dispute resolution queue: Centralized case management for escalated consumer and merchant disputes. Supports SLA tracking and audit trails.

MVP vs Full-Scale: What BNPL Features to Build First

Every feature above belongs in your roadmap. What changes is the order. Here’s how to phrase it.

| Feature | MVP (3–5 months) | Full-scale (8–12 months) |

| KYC & onboarding | Basic ID + soft credit pull | Biometric + liveness + bureau integration |

| Credit decisioning | Rule-based scoring model | AI/ML engine with alternative data |

| Virtual card | – | Visa/Mastercard network integration |

| Installment options | Pay-in-4 only | Pay-in-4, Pay-in-30, long-term plans |

| Merchant integration | Single platform (Shopify) | Multi-platform + POS + full API/SDK |

| Fraud detection | Basic rule-based flags | ML anomaly detection + device fingerprinting |

| Compliance | Single market | Multi-jurisdiction automated reporting |

| Multi-currency | – | Global currencies + FX handling |

Tech Stack for Buy Now Pay Later App Development

The recommended tech stack for a BNPL platform is React Native or Flutter (frontend), and Node.js or Python (backend).

For a BNPL product, tech stack choices directly affect three things:

- How fast does the app approve shoppers at checkout?

- How well does it scale as transaction volume grows? and

- How easily does it meet financial regulations across markets?

Here’s the full recommended stack for a production-grade BNPL platform:

| Layer | Recommended tools | Why it matters for BNPL |

| Frontend | React Native, Flutter, Swift / Kotlin | Cross-platform builds cut time and cost. Native is faster for high-performance checkout flows. |

| Backend | Node.js, Python (Django), Java (Spring Boot) | Java and Python handle high-throughput credit decisioning. Node.js suits real-time flows. |

| Database | PostgreSQL, MongoDB, Redis | PostgreSQL for structured financial records. MongoDB for flexible user data. Redis for session caching and millisecond credit decision speed. |

| Payment gateways | Stripe, Adyen, Braintree, PayPal | Stripe and Adyen offer the most mature BNPL-compatible rails. Sandbox all integrations before going live. |

| Credit bureaus | Experian API, Equifax API, TransUnion API | Real-time credit pulls power your approval engine. Combine bureau data with alternative data signals for more accurate scoring. |

| Cloud & DevOps | AWS, GCP, Docker, Kubernetes | Auto-scaling is non-negotiable. Transaction spikes during retail events can multiply volume 10x in minutes. |

| Security | TLS 1.3, AES-256, OAuth 2.0 MFA | PCI-DSS mandates encryption at rest and in transit. MFA and OAuth protect both consumer accounts and admin access. |

| AI / ML | TensorFlow, scikit-learn, AWS, SageMaker | Powers proprietary credit scoring models and real-time fraud detection. Improves default prediction accuracy beyond bureau scores alone. |

One architectural decision worth calling out separately

Your credit decisioning layer needs to return approvals in under 500 milliseconds. That’s the threshold where checkout abandonment spikes.

BNPL Compliance and Regulatory Requirements

BNPL products handle lending, payments, and customer data at the same time. That mix places your platform under financial and privacy regulations across multiple regions.

Regional BNPL Compliance Requirements

In the US, you need to review CFPB guidance, state lending rules, and Truth in Lending Act (TILA) disclosures. Global markets also enforce strict standards through the FCA, ASIC, and MAS.

| Region | Key Requirements |

| United States | CFPB oversight, state lending licenses, TILA disclosures |

| United Kingdom | FCA authorization, Consumer Credit Act compliance |

| Europe | Customer Due Diligence (CDD) II lending rules, GDPR data protection |

| UAE & Saudi Arabia | CBUAE and SAMA regulatory approvals |

| Asia-Pacific | MAS, RBI, and ASIC lending and payment frameworks |

Pre-Launch BNPL Compliance Checklist

These are the common fintech development challenges that cause the most expensive delays when discovered late. Work through this list before your first production deployment:

| Compliance Area | Purpose |

| KYC and AML checks | Reduce fraud and verify customer identity |

| PCI-DSS controls | Protect payment and cardholder data |

| GDPR and privacy workflows | Manage consent and customer data securely |

| TILA disclosures | Explain fees and repayment terms clearly |

| SOC 2 Type II readiness | Meet enterprise security expectations |

| Vendor compliance reviews | Reduce third-party operational risk |

| Legal review before launch | Prevent delays during scaling |

Every BNPL Market Has Different Rules

Tell us your target markets and our experts will map the compliance, licensing, and technical architecture requirements for each region—helping you build with confidence from day one.

Start Your BNPL Discovery Session →Industries Where BNPL Is Disrupting the Market

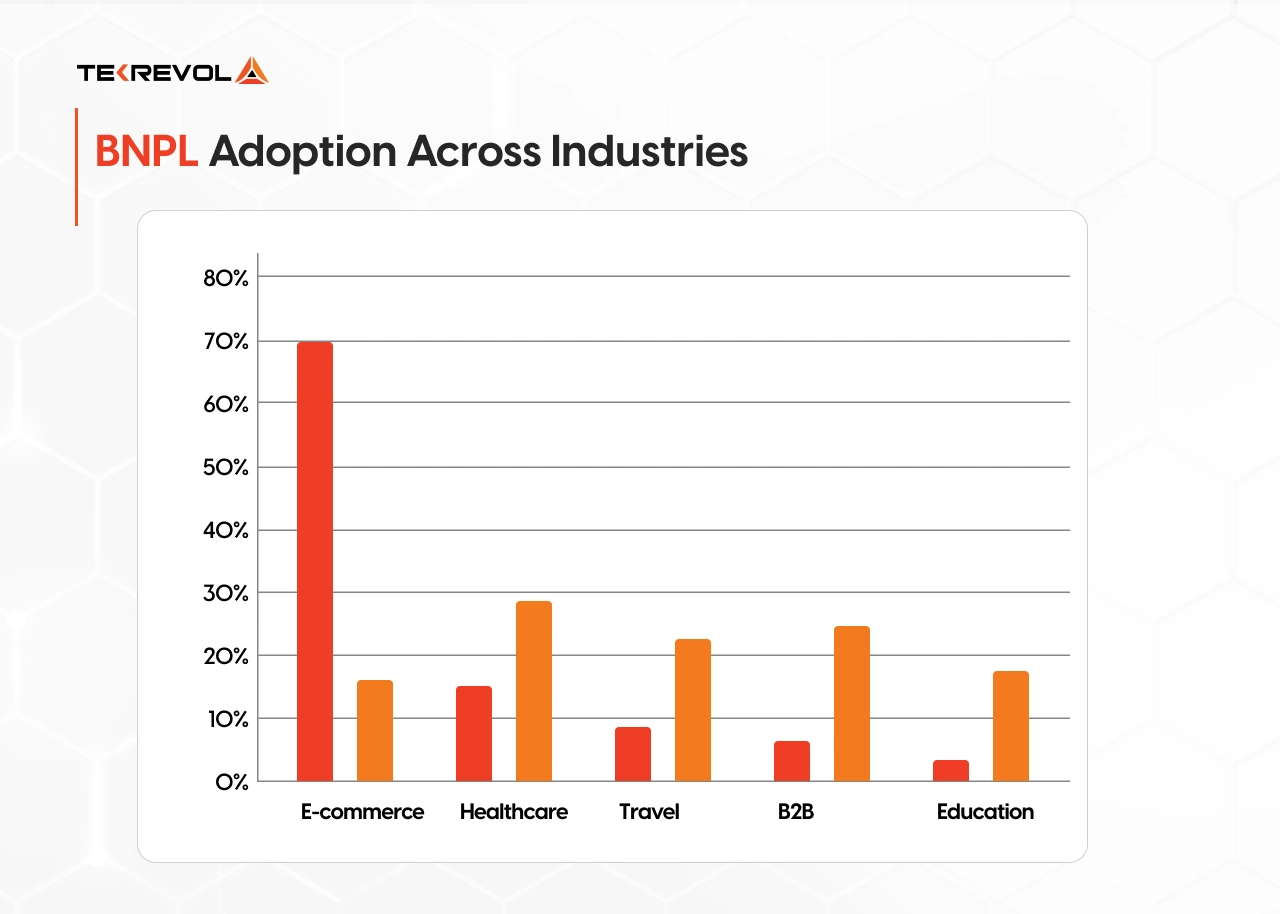

The demand for Buy Now Pay Later app development is active across five major verticals: e-commerce, healthcare, travel, B2B procurement, and education.

Started in retail, BNPL has moved into every major spending category. Healthcare, travel, and B2B BNPL are growing fastest, with healthcare adoption projected to grow at a 29.7% CAGR through 2030. (Source: Mordor Intelligence)

Anywhere consumers face high upfront costs and prefer to pay over time, BNPL follows.

E-commerce

E-commerce is where BNPL started and still drives the highest transaction volumes globally. Merchants that offer it at checkout see up to 85% higher average order values. Up to 40% of those purchases come from customers who are new to the retailer. Today, e-commerce app development services need to build BNPL into the checkout experience from the start.

Healthcare

Healthcare is BNPL’s fastest-growing vertical outside retail. Patients face growing out-of-pocket costs for elective procedures, dental work, and wellness services. Many of these fall outside standard insurance coverage. A healthcare app development Company and BNPL turns those costs into manageable installments without requiring patients to carry credit card debt.

Travel

One in ten Americans now uses BNPL to pay for travel and vacations. Flights, hotels, package tours, and experiences are high-ticket and time-sensitive purchases. Installment payment changes buying behavior in this category specifically. Platforms like Uplift pioneered this model, partnering with airlines and travel agencies to embed BNPL at the booking stage.

Education

Education BNPL is gaining traction across tuition installment plans, online course access, and professional certification programs. Learners who want access to high-value education without paying up front are a growing segment for BNPL providers. Ed-tech software solutions that embed BNPL at enrollment report higher course completion rates and lower drop-off at the payment step.

B2B procurement

B2B BNPL is the least crowded vertical in the space right now. Businesses use it to finance procurement, manage cash flow gaps, and fund equipment purchases without drawing on existing credit lines. Average B2B transaction values run well above consumer BNPL levels. That translates to higher merchant fees and stronger unit economics for platform providers.

Challenges in BNPL App Development and How to Solve Them

A BNPL platform comes with a specific set of challenges. Fraud detection, multi-market regulatory fragmentation, and merchant adoption friction are the most prevalent challenges that standard payment products do not face.

Here are roadblocks that affect leading BNPL providers globally and how to address each one.

Credit risk and default management

BNPL default rates average 1.8 to 2 percent globally. Late payment rates run as high as 41 percent. Managing the gap between those two numbers is one of the hardest problems in BNPL product design.

Solution

Start with a rule-based credit scoring model. As repayment data grows, migrate to an ML model. Set dynamic credit limits that adjust based on each user’s repayment behavior over time.

Fraud detection

BNPL’s fast, frictionless approval process creates an opening for identity fraud and synthetic identity attacks. Fraudsters exploit the gap between soft credit checks and real-time purchase approval.

Solution

Layer biometric authentication into onboarding. Add device fingerprinting to flag account access from unfamiliar devices. Deploy ML-based anomaly detection to surface unusual transaction patterns in real time.

Multi-market regulatory fragmentation

Compliance requirements vary across every major market. A product built for the US needs significant re-engineering to operate in the UK, UAE, or Singapore.

Solution

Build a modular compliance layer that can flex by jurisdiction without requiring a platform rebuild. This approach avoids the costly re-architecture teams face when they try to scale globally.

Merchant adoption friction

BNPL only generates revenue when merchants accept it. Many merchants delay integration because the technical lift feels too high relative to the expected conversion lift.

Solution

Build a well-documented SDK that integrates in hours. Provide a sandbox environment for testing before going live. Offer a dedicated integration support team for your first merchant cohort.

Scaling Under Transaction Spikes

BNPL volume doesn’t grow linearly. Retail events: Black Friday, holiday seasons, flash sales can multiply transaction load 10x overnight. Without automation, dispute handling alone can consume up to 10% of annual OPEX as adoption scales.

Solution

Build on auto-scaling cloud infrastructure from day one. Stress-test your system before launch, not after your first traffic spike.

Why Choose TekRevol for BNPL App Development

Building a BNPL product means navigating payments, lending, compliance, and fraud prevention all at once. That’s different from a standard app. As an experienced fintech app development company, TekRevol understands such financial product architecture.

We have shipped regulated lending and payment products across the US, UK, and MENA. Our experts have navigated CFPB audits, FCA authorization processes, and CBUAE licensing requirements on behalf of clients, on live products.

If you’re scoping a build, start with a free consultation. We’ll map your BNPL app development architecture, flag your compliance requirements, and give you a realistic scope before you commit.

Ready to Build a BNPL App That Scales?

Get a compliance-first development plan tailored to your target markets, business goals, and launch timeline. TekRevol helps you build secure, scalable BNPL solutions designed for long-term growth.

Start Your Project with TekRevol →