- Cash advance app development requires a payroll API, banking infrastructure, KYC layer, and ACH payment rails, all built in sync.

- A production-ready cash advance MVP costs $65,000–$100,000 and takes 10–14 weeks with the right development partner.

- Model your revenue on tips and transfer fees. Mandatory charges classify your product as a loan under federal law.

- The CFPB’s December 2025 ruling protects EWA products, but only if you charge zero mandatory fees and advance already-earned wages.

- Missouri and Nevada are your soft launch states. California, New York, and Texas require a dedicated legal review before entry.

78% of Americans live paycheck to paycheck.

Earnin turned that into a $421M+ funded business. Not by offering loans, but by giving workers early access to wages they already earned.

And people are asking: “Can I build something like this?”

Yes. But it’s not as simple as building a payment app and slapping a “get paid early” label on it.

Cash advance app development entails navigating banking partnerships, payroll API integrations, KYC verification, and a regulatory environment in which the CFPB is actively rewriting the rules. Miss any of it, and you’re either non-compliant, unfundable, or both.

Most founders discover this too late, after they’ve already spent months building the wrong thing. The ones who get it right start with an experienced mobile app development company that understands financial regulations, banking infrastructure, and compliance architecture.

This guide covers exactly how to build a cash advance app or earned wage access platform in 2026, including the features, compliance requirements, banking integrations, and real development costs.

So, let’s dive in!

What Is a Cash Advance App, & And Why Is It Not a Payday Loan?

A cash advance app gives workers access to money they’ve already earned, before payday hits. A payday loan lends money against future income. That difference changes everything.

Here’s the three-way breakdown founders need to understand before writing a single line of code:

Earned Wage Access (EWA): The user accesses wages they’ve already worked for. No interest. No loan agreement. Repayment comes automatically from their next direct deposit. Earnin runs on this model.

Cash Advance: A short-term advance against expected income. May or may not carry fees. The term is used loosely; some apps use it to describe EWA, others use it for something closer to a micro-loan.

Payday Loan: A loan against future income, with interest rates that can hit 400% APR. Heavily regulated. Actively targeted by the CFPB. Not what you want to build.

Why does this distinction matter so much? Because it determines:

- Whether you need a lending license

- Whether your banking partner will work with you

- Whether the CFPB classifies your product as a loan

- Whether VCs will fund you

Earnin cracked the code by framing its product as EWA, not lending. Tip-based. No mandatory fees. No recourse if a user doesn’t repay. That framing kept it out of predatory lending regulations and made it fundable.

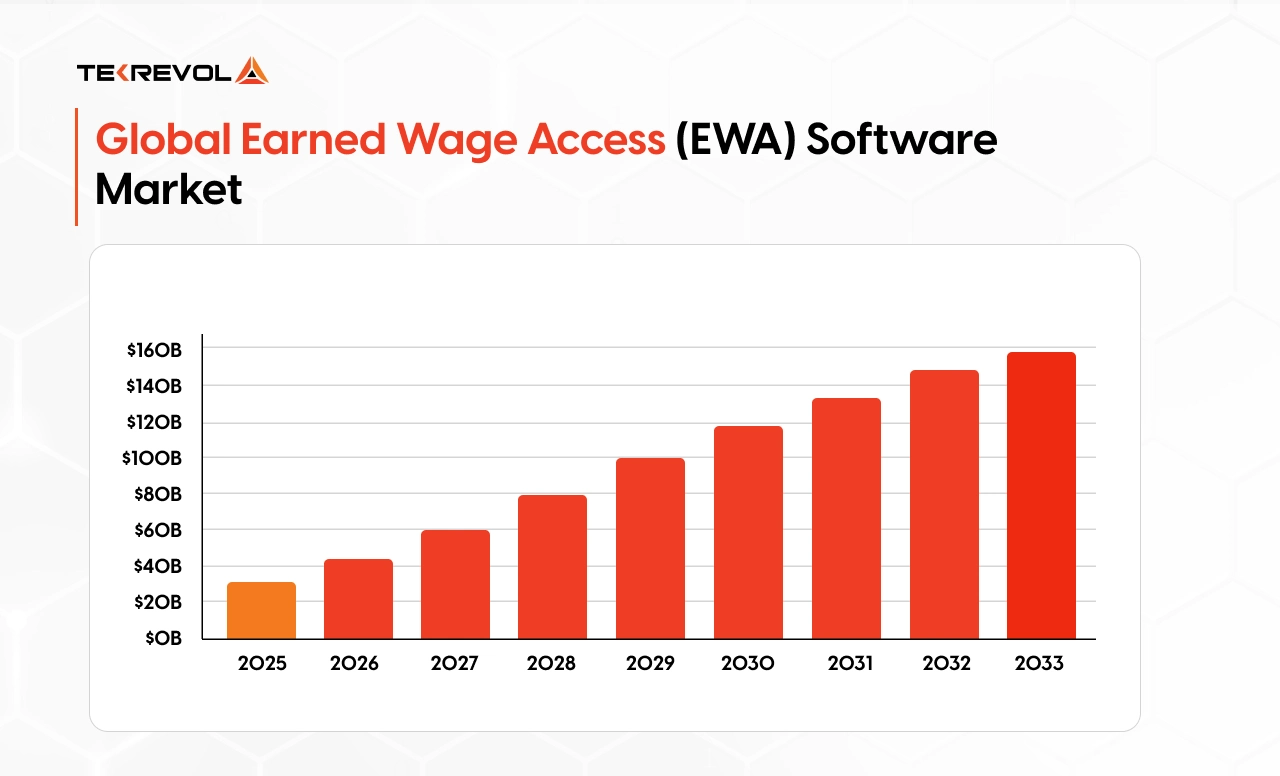

The global Earned Wage Access (EWA) software market was valued at USD 29.94 billion in 2025 and is projected to grow to USD 156.45 billion by 2033. Whether you are pursuing full Earnin clone app development or building an original EWA product, the window is open. But only if you build it right.

How Earnin’s Model Actually Works

It’s a simple loop, but the infrastructure behind it is anything but simple.

- User downloads the app and signs up.

- Links their bank account via Plaid.

- Connects their employment data via payroll API or GPS work-hour tracking.

- App verifies income patterns and calculates the available advance

- User requests an advance of up to $150/day, $750/pay period for standard users. Earnin’s Live Pay feature allows employees to stream their earned wages in real time, with access to up to $1,500 per pay period.

- Funds hit via standard ACH (free, 1–3 days) or Lightning Speed ($2.99–$5.99, instant)

- On payday, the advance is auto-debited from their bank account.

But behind that simple UX is a Plaid integration, a payroll API connection, an AI risk engine, an ACH origination pipeline, and a compliance layer that took years to build. That’s what you’re actually building. And getting it right means working with a team that delivers production-grade API integration services, not just connecting endpoints, but building the financial infrastructure your product runs on.

Core Features Every Cash Advance App Needs

A modern cash advance app depends on secure banking integrations, compliance systems, automated repayments, and real-time risk analysis to function smoothly. From identity verification to instant payouts, each feature plays a critical role in delivering a fast, secure, and compliant user experience. Here’s what each one requires.

| Core feature | Purpose | Key Technologies & Providers |

| KYC & User Onboarding | Verifies identity and prevents fraud during signup | Jumio, Onfido, Persona, Socure |

| Bank Account Linking | Connects user bank accounts to access balances and transaction data | Plaid, Yodlee, MX |

| Income Verification | Confirms employment and recurring income patterns | Argyle, Pinwheel, Plaid |

| Risk & Eligibility Engine | Calculates safe advance limits using financial behavior data | AI underwriting models, transaction analytics |

| ACH & Instant Transfers | Sends funds through standard or instant payment rails | Stripe Treasury, Dwolla, FedNow, RTP |

| Repayment Automation | Schedules automatic repayment on payday | ACH debit systems, bank APIs |

| Transaction History | Displays advances, repayments, and account activity | Financial dashboards, reporting systems |

| Balance Alerts & Insights | Helps users track spending and avoid overdrafts | Budgeting tools, analytics engines |

| Fraud Detection & Security | Monitors suspicious activity and protects accounts | Socure, Sift, Alloy |

| Customer Support | Enables in-app support and dispute handling | Zendesk, Intercom |

| Cloud & BaaS Infrastructure | Powers scalability, security, and banking operations | AWS, Unit, Synctera, Treasury Prime |

To get a deeper look at these features, check out our complete guide on 10 Must-Have Features for Fintech App Development in 2026

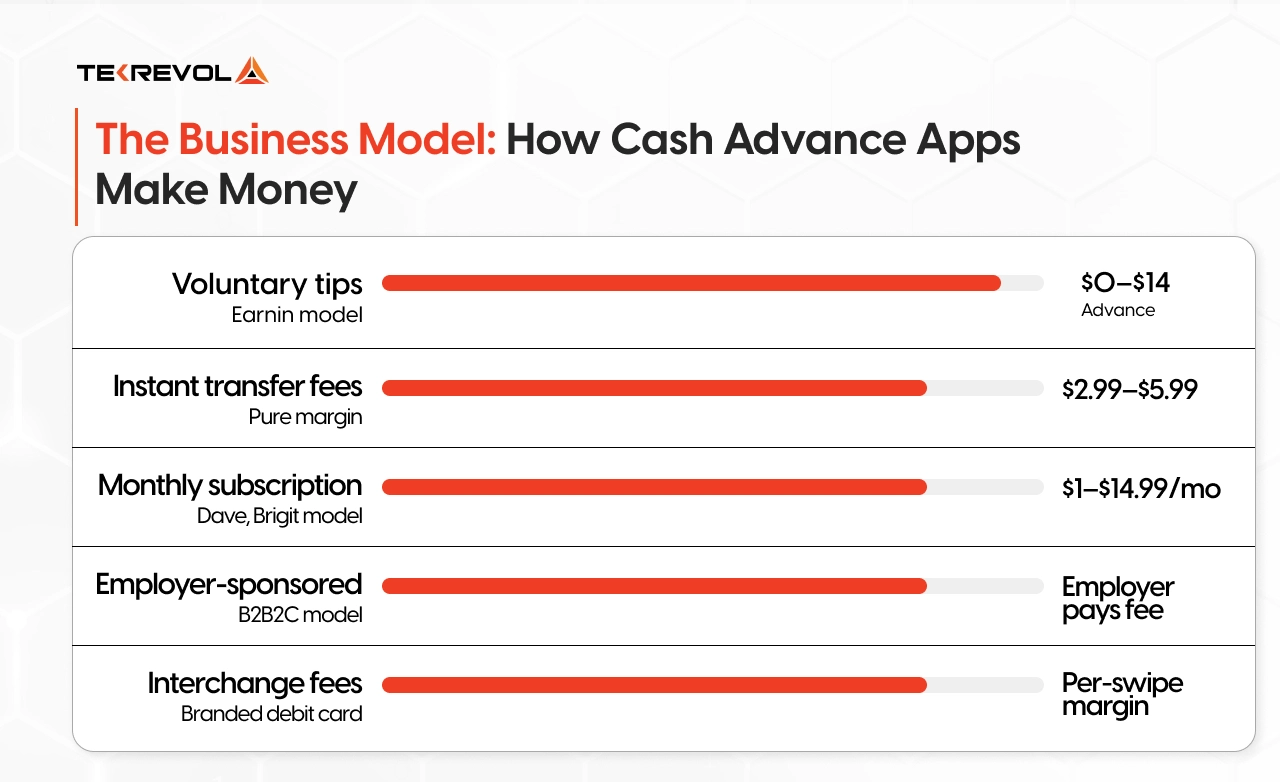

The Business Model: How Cash Advance Apps Make Money

Cash advance apps make money through tips, subscription fees, instant transfer fees, and employer-sponsored programs, not interest.

This is the first thing investors will ask. Know your revenue model before you start the build.

Here’s how the major models work:

Voluntary Tips (Earnin model)

Users choose what to tip, anywhere from $0 to $14. Sounds risky. But Earnin built a billion-dollar business on it. The psychology works: people pay what feels fair when the service genuinely helps them.

Monthly Subscription Fees

Dave charges $1/month. Brigit charges $9.99–$14.99/month. Users pay for access to advances, budgeting tools, and overdraft alerts. Predictable recurring revenue is easier to model for investors.

Express Transfer Fees

Standard ACH is free but slow. Instant transfers cost $2.99–$5.99 per transaction. This is pure margin. Users who need money right now will pay for it every time.

Employer-Sponsored EWA (B2B2C)

Companies like DailyPay and PayActiv sell EWA as an HR benefit. The employer pays the platform fee. Employees get free access. Lower default risk because payroll data is verified directly.

Interchange Fees

If your app issues a branded debit card, you earn interchange on every swipe. MoneyLion built a significant revenue stream here.

Affiliate Revenue

Recommend a credit card, insurance product, or savings account, and earn a commission when users sign up.

B2C vs B2B2C: Which Cash Advance Model Should You Build

It depends on your go-to-market strategy.

B2C (consumer-direct): Faster to launch. No enterprise sales cycle. But income verification is hard;r, you’re relying on Plaid data and payroll APIs rather than direct employer confirmation. Default risk is higher.

B2B2C (employer-integrated): Slower to scale. You need to close employer contracts first. But your income data is cleaner, your default rate is lower, and your unit economics are better. This is the model attracting the most institutional capital right now.

Most successful platforms start B2C to prove the product, then layer in B2B2C as they scale.

| Factor | B2C (Consumer-Direct) | B2B2C (Employer-Integrated) |

| Income Verification | Harder relies on Plaid transaction data and payroll APIs | Cleaner, the employer confirms payroll directly |

| Default Risk | Higher, no direct employer confirmation | Lower, repayment comes straight from payroll |

| Time to Launch | Faster, no enterprise sales cycle required | Slower, requires closing employer contracts first |

| Revenue Model | Tips, subscriptions, and instant transfer fees | Employer-paid platform fees, employee access is free |

| Capital Requirements | Lower upfront, higher default reserves needed | Higher upfront for sales and onboarding, better unit economics long term |

Compliance & Regulatory Requirements

Compliance is the part most founders underestimate, and the one that kills the most products. Here’s everything you need to get right before launch.

CFPB & the Regulatory Landscape

On December 23, 2025, the CFPB issued its most important EWA ruling yet.

The advisory opinion confirmed that qualifying EWA products are not “credit” under the Truth in Lending Act, and that optional delivery fees and voluntary tips are not “finance charges” under Regulation Z. This reversed a 2024 Biden-era rule that would have classified most EWA products as loans.

But it’s not a blanket green light. To qualify as “Covered EWA,” your product must:

- Only advance wages already earned, not future income

- Repay through employer-facilitated payroll deduction

- Charge no mandatory fees

- Use no aggressive repayment collection

One wrong design decision in your fee structure or repayment flow, and you cross into loan classification territory. That means APR disclosures, TILA obligations, and state lending licenses.

The window is open. But the definition of compliant is precise. Get a fintech app development company involved before you write a single line of code.

State Lending License Requirements

Federal guidance sets the floor, but states set the ceiling. There is no single national law governing cash advance apps, which means your ability to operate legally varies dramatically depending on where your users live. Skipping this step isn’t a gray area; it’s how apps get shut down.

Some states have created favorable frameworks for compliant products:

- Missouri and Nevada have passed legislation providing clear, manageable pathways for cash advance apps.

- These states are ideal for a soft launch before pursuing national expansion

Other states require significantly more groundwork:

- California may require a money transmitter license or a lending license, depending on how your product is structured

- New York’s Department of Financial Services has sweeping authority over fintech products operating in the state

- Texas has complex short-term lending oversight that warrants dedicated legal review before market entry

Launch in favorable states first, build your compliance track record, then expand state by state with legal counsel. A 50-state rollout on day one is how compliance debt accumulates fast.

KYC & AML Compliance

The moment your app moves money, federal identity and anti-money laundering requirements apply, no exceptions. KYC and AML aren’t features you add later. They are the infrastructure your entire transaction flow must be built on top of.

KYC requirements mean your app must, before issuing any advance:

- Verify each user’s identity using a government-issued ID

- Screen users against OFAC and other federal watchlists

- Store and maintain identity records available for regulatory audit

- Re-verify identity if significant account details change

AML requires ongoing operational discipline beyond onboarding:

- Continuously monitor transactions for suspicious patterns

- File Suspicious Activity Reports with FinCEN when required thresholds are triggered

- Maintain a written, documented AML compliance program

- Designate a qualified compliance officer within your organization

Tools like Jumio, Onfido, Persona, and Socure handle all of this automatically via API. The most common mistake is treating KYC as a one-time onboarding step; real compliance requires continuous monitoring throughout the entire user lifecycle.

Data Security: SOC 2, Encryption & Privacy Standards

Cash advance apps sit on some of the most sensitive personal and financial data that exists. Your banking partners and BaaS providers know this, and they will require documented proof of your security posture before they agree to work with you. Meeting these standards isn’t about checking boxes. It’s the price of entry.

Four standards apply to virtually every cash advance app:

- SOC 2 Type II: Demonstrates your security controls are consistent, tested, and independently audited over time. Required by most BaaS providers before they’ll onboard you

- PCI-DSS: Mandatory if your app processes, stores, or transmits card data in any form

- GLBA: Requires the protection of users’ non-public personal information and a clear published privacy policy

- State Privacy Laws: Build to CCPA standards from day one, and you’ll be ahead of most other state requirements automatically

Your technical infrastructure must include:

- AES-256 encryption for all data at rest and in transit

- OAuth 2.0 for secure API authentication

- Multi-factor authentication and biometric login for all users

- SSL/TLS across every data transmission point

- Scheduled penetration testing and regular vulnerability assessments

Security built in from the start is dramatically cheaper than retrofitting it under pressure from a banking partner audit.

Get a Free Compliance Review Before You Build

Our fintech specialists will help you structure your cash advance app correctly from the start, identifying key compliance requirements, risk factors, and regulatory considerations before development begins.

Book A FREE Call Now!Banking Infrastructure & API Integrations

To build a cash advance app or payroll advance app development project, you need four infrastructure layers: a BaaS provider for banking operations, Plaid for bank verification, a payroll API for income verification, and an ACH/instant payment rail for fund movement.

Here’s what each layer looks like in production:

Layer 1: Banking-as-a-Service (BaaS)

BaaS providers give you access to core banking infrastructure without needing a bank charter of your own. They sit between you and the regulated banking system, handling tasks such as account creation, funds holding, and transaction processing on your behalf.

The three main players in this space are:

- Unit: Best for fintech startups. Known for fast onboarding and strong built-in compliance tooling

- Synapse: Built for scale-stage platforms that need a broad banking partner network

- Column: Best for technical teams that want more control. The column holds its own bank charter, which means fewer middlemen and more flexibility.

Layer 2: Bank Account Verification

Before you can advance money to a user, you need to verify their bank account. This confirms the account is real, active, and belongs to them.

- Plaid is the industry default and the most widely integrated option

- Yodlee and MX are solid alternatives used for redundancy or where Plaid coverage is limited

Layer 3: Payroll & Income Verification

Cash advance apps need to confirm that a user actually has income coming in before issuing an advance. Payroll APIs connect directly to employers and payroll systems to pull that data in real time.

- Argyle: Provides real-time employment and payroll data with a growing employer network.

- Pinwheel: Strong payroll connectivity, already used by several major neobanks

Layer 4: ACH & Instant Payment Rails

This is how money actually moves from your platform to the user’s bank account. Speed matters here because users requesting a cash advance typically need funds quickly.

- Stripe Treasury: The easiest integration path for early-stage products already using Stripe

- Dwolla: Built specifically for ACH transfers, well-suited for high-volume operations.

- FedNow: The Federal Reserve’s instant payment network, now the widely adopted standard for real-time transfers across US banking in 2026, with over 1,000 financial institutions live on the network and growing adoption, making it the default expectation for any serious cash advance platform

Layer 5: KYC Providers

Before any money moves, you are legally required to verify who your user is. KYC providers handle identity verification automatically, so you don’t have to build it yourself.

- Jumio, Onfido, Persona, and Socure are the leading options

- Your choice depends on your transaction volume, the geographies you operate in, and your specific compliance requirements

Tech Stack for a Cash Advance App

Choosing the right tech stack for a cash advance app is a business and compliance decision, not just a technical one. Every layer must handle financial data securely, integrate with regulated banking infrastructure, and scale as your user base grows. Here is what a production-grade stack looks like.

| Layer | Technology | Why This Choice |

| Mobile Frontend | React Native / Flutter | Single codebase for iOS and Android cuts development time and cost in half — critical for an MVP budget |

| Backend | Node.js / Python (Django) | Node.js handles high-concurrency payment events efficiently; Django brings built-in security defaults that matter in a regulated environment |

| Database | PostgreSQL | Relational structure is essential for financial data, transaction integrity, audit trails, and complex joins that MongoDB simply cannot handle reliably |

| Banking-as-a-Service | Unit / Synapse / Column | Gives you core banking infrastructure without a bank charter, the only practical path for a fintech startup |

| Bank Linking | Plaid | Industry default with the widest bank coverage in the US and pre-built compliance tooling |

| Income Verification | Argyle / Pinwheel | Direct payroll connectivity gives you cleaner income data than screen-scraping or transaction analysis alone |

| ACH & Payments | Stripe Treasury / Dwolla | Stripe for early-stage simplicity; Dwolla for high-volume ACH operations at scale |

| KYC & Identity | Jumio / Persona / Onfido | Automated identity verification with built-in OFAC screening is required before any money moves |

| Cloud Infrastructure | AWS / Google Cloud | Enterprise-grade security, SOC 2 compatible infrastructure, and the scaling headroom a payments platform needs |

| Security | AES-256, OAuth 2.0, MFA | The minimum encryption and authentication standard that any banking partner will require before approving you |

How to Build a Cash Advance App Like Earnin?

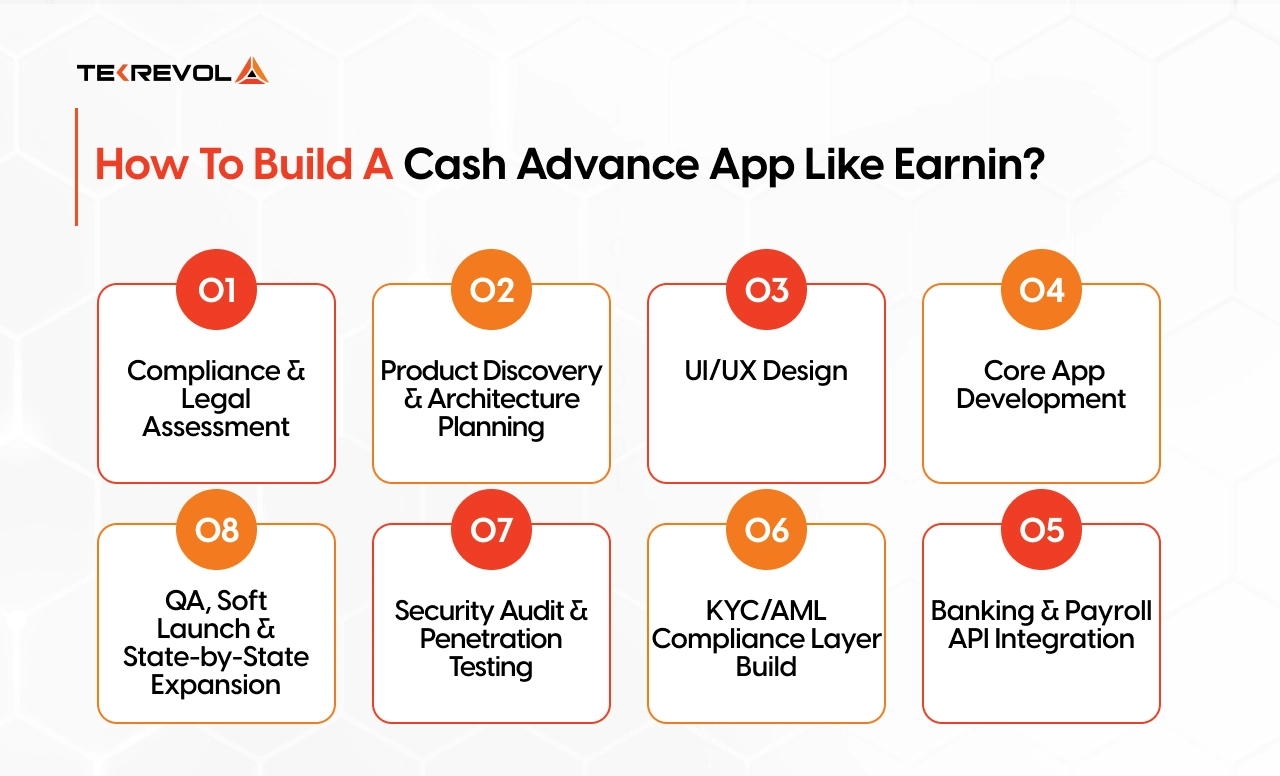

Building a cash advance app takes 8 defined steps, from compliance assessment to launch. Here’s the exact roadmap TekRevol follows for earned wage access app development.

Step 1: Compliance & Legal Assessment

Estimated Cost: $5,000–$10,000 | Timeline: 1–2 weeks

Before a single wireframe. Before a single API call. Before anything. You need to know what you’re legally allowed to build, and where.

This step covers:

- EWA vs loan classification under CFPB guidance

- State-by-state licensing requirements for your target markets

- Fee structure review: Does your monetization model keep you in EWA territory?

- KYC/AML program requirements

- Data privacy obligations (CCPA, GLBA)

Skipping this step is the most expensive mistake in fintech. Founders who skip it build the wrong product, then spend 3x more fixing it after a banking partner or regulator pushes back.

Step 2: Product Discovery & Architecture Planning

Estimated Cost: $5,000–$10,000 | Timeline: 1–2 weeks

Now you define what you’re building, and how it fits together technically.

This step covers:

- User journey mapping (onboarding → advance → repayment)

- Feature prioritization, MVP vs phase 2

- BaaS provider selection (Unit, Synapse, Column)

- Payroll API selection (Argyle vs Pinwheel)

- KYC provider selection (Jumio, Onfido, Persona)

- Database and cloud infrastructure decisions

- Microservices vs monolith decision (hint: go microservices)

The output is a detailed technical spec your dev team can actually build from. Not a deck. Not a vision doc. A real architecture blueprint.

Step 3: UI/UX Design

Estimated Cost: $8,000–$15,000 | Timeline: 2–3 weeks

Financial apps live or die on trust. And trust starts with design.

73% of fintech users abandon an app within the first week. Most of that happens because the onboarding feels confusing, slow, or sketchy. Your design has to communicate security and simplicity at the same time.

This step covers:

- User onboarding flow (KYC screens, bank linking, consent flows)

- Dashboard design (available advance, balance, repayment date)

- Advance request and confirmation flow

- Transaction history and statements

- Push notification design

- Accessibility and mobile responsiveness

The rule: every extra tap is a user you’re losing. Design for the person who needs money right now, not someone leisurely browsing a fintech app.

Step 4: Core App Development

Estimated Cost: $40,000–$80,000 | Timeline: 6–10 weeks

This is where the product gets built. Frontend, backend, database, all of it.

This step covers:

- User registration and authentication system

- KYC onboarding flow (integrated with Jumio, Onfido, or Persona)

- Bank account linking via Plaid

- Income verification via Argyle or Pinwheel

- AI risk engine for advanced eligibility calculation

- Advance request and approval logic

- Admin dashboard for operations and compliance monitoring

- Push notification system

- Transaction history and statements module

This is also where architecture decisions from Step 2 pay off, or come back to hurt you. A well-scoped architecture makes this phase predictable. A poorly scoped one turns into a constant rebuild.

Step 5: Banking & Payroll API Integration

Estimated Cost: $10,000–$20,000 | Timeline: 3–4 weeks

This is the most technically complex step. And the one most dev shops underestimate.

You’re not just calling an API. You’re integrating with live financial infrastructure that has strict uptime, security, and compliance requirements.

This step covers:

- BaaS provider integration (Unit, Synapse, or Column)

- Plaid integration for bank account verification and transaction data

- Argyle or Pinwheel integration for payroll and employment data

- ACH origination setup — standard and instant transfer rails

- FedNow integration for real-time payment settlement

- Webhook configuration for real-time transaction events

- Fallback logic if any integration fails

Every integration needs sandbox testing before it touches real user data. Then staging. Then production. Don’t rush this phase.

Step 6: KYC/AML Compliance Layer Build

Estimated Cost: $8,000–$15,000 | Timeline: 2–3 weeks

KYC isn’t just a signup screen. It’s an ongoing compliance system.

This step covers:

- Automated identity verification workflow (document scan → biometric match → OFAC screening)

- Ongoing transaction monitoring for AML flags

- Suspicious Activity Report (SAR) filing workflow

- BSA compliance program implementation

- Adverse media and politically exposed persons (PEP) screening

- Audit log system for regulatory review

- Compliance officer dashboard

The mistake most teams make: they treat KYC as a one-time onboarding event. Real AML compliance is continuous; every transaction is monitored, not just the first one.

Step 7: Security Audit & Penetration Testing

Estimated Cost: $10,000–$20,000 | Timeline: 2–3 weeks

Your banking partner will ask for this before approving you. Do it before they ask.

This step covers:

- SOC 2 Type II readiness assessment

- Penetration testing across all API endpoints

- Vulnerability scanning — frontend, backend, database

- Encryption audit (AES-256 at rest, TLS in transit)

- Authentication review (OAuth 2.0, MFA, session management)

- OWASP Top 10 security checks for mobile and web

- PCI-DSS compliance check if card data is in scope

- Remediation of any findings before launch

This isn’t a formality. EWA apps hold bank account credentials, SSNs, and income records. One breach ends your product and your reputation simultaneously.

Step 8: QA, Soft Launch & State-by-State Expansion

Estimated Cost: $8,000–$15,000 | Timeline: 2–4 weeks

Don’t launch everywhere at once. Launch smart.

This step covers:

- Functional QA across all user flows

- Performance testing under simulated load

- Regulatory QA: Does every flow comply with your target states’ requirements?

- UAT with a closed beta group

- Soft launch in EWA-friendly states (Missouri, Nevada)

- Monitoring and iteration based on real user behavior

- State-by-state expansion plan with legal review at each stage

The soft launch phase is where you find out what your risk engine gets wrong. Better to find that out with 500 users in Nevada than 50,000 users in California.

Not Sure What Your Cash Advance App Will Cost?

Get a free estimate from TekRevol within 48 hours, tailored to your feature set, compliance requirements, integrations, and target launch states—so you can plan with confidence.

Get My Free Estimate!Cash Advance App Development Cost

Understanding fintech app development cost is the first step every founder needs to take before scoping a build. Total development cost for a cash advance app ranges from $65,000 for a basic MVP to $400,000+ for an enterprise-grade EWA platform

| Build Component | Cost Range | Timeline |

| Discovery & Compliance Assessment | $5,000–$10,000 | 1–2 weeks |

| UI/UX Design | $8,000–$15,000 | 2–3 weeks |

| EWA MVP (core features) | $60,000–$100,000 | 6–10 weeks |

| Full Platform with AI Risk Engine | $120,000–$200,000+ | 16–24 weeks |

| BaaS Integration & Banking Setup | $10,000–$20,000 | 3–4 weeks |

| KYC/AML Compliance Layer | $8,000–$15,000 | 2–3 weeks |

| Security Audit (SOC 2 prep) | $10,000–$20,000 | 2–3 weeks |

| Legal & Licensing Fees | $15,000–$50,000+ | 3–6 weeks |

Why Choose TekRevol for Cash Advance App Development

Building a cash advance app means navigating banking partnerships, payroll integrations, KYC verification, and a regulatory environment that actively penalizes missteps. TekRevol has worked with fintech founders at every stage, delivering 100+ fintech and mobile app projects across payments, neobanking, and earned wage access platforms, from pre-seed startups validating their first MVP to scaling platforms expanding state by state.

We know where cash advance breaks down. Fee structures that accidentally cross into loan classification. Payroll API integrations that fail compliance review. KYC systems are built as a one-time onboarding step instead of continuous monitoring. Our team has seen these mistakes firsthand and built the processes to prevent them.

What TekRevol Brings to Your Cash Advance Build:

- Cash Advance Compliance Architecture: We structure your fee model, repayment flow, and KYC system to meet CFPB’s Covered EWA definition from day one

- Banking & Payroll API Integration Services: Hands-on experience with Plaid, Argyle, Pinwheel, Unit, Dwolla, and FedNow across production cash advance deployments

- AI-Powered Risk & Eligibility Engine: Custom advance limit and underwriting models built specifically for cash advance and EWA platforms

- Full-Cycle Product Delivery: From compliance assessment and architecture through soft launch, state-by-state expansion, and post-launch iteration

Get Your Free Cash Advance App Roadmap — Worth $500

Speak with our fintech specialists to receive a tailored development roadmap, compliance checklist, feature strategy, and cost estimate designed specifically for your cash advance app concept.

Claim My Free Roadmap Now!