- Fintech app development in Austin costs $60,000–$350,000+ in 2026, driven by compliance, integrations, and application complexity.

- Compliance, not UI, drives fintech app costs, with PCI-DSS, SOC 2, and KYC/AML adding 20–35% to development expenses.

- Austin fintech founders increasingly reduce costs by integrating proven compliance infrastructure instead of building financial systems from scratch.

- Texas has no state income tax, a real, practical advantage that’s pulling fintech founders and senior engineering talent to Austin specifically, not just tech talent generally.

- TekRevol fintech software development across banking, wallets, payments, and wealth management, with most financial projects ranging from $10,000–$199,999.

Fintech app development in Austin costs $60,000 to $350,000+ in 2026. Where your project lands depends far less on your feature list than most founders expect, and far more on one decision: are you building financial infrastructure from scratch, or are you integrating proven, pre-compliant rails underneath your own product experience? Get that decision right and you can launch in months. Get it wrong and you’ll spend your first year of runway rebuilding compliance architecture that already existed off the shelf.

This guide breaks down what actually drives fintech app development cost, what compliance realistically requires, and why Austin’s own fintech ecosystem, smaller than its AI and healthtech scenes, is quietly showing the rest of the country how to build fintech products faster.

Scoping a fintech build and want a realistic budget before you talk to investors?

Talk to TekRevol's fintech development team for an itemized estimate within 48 hours.

Get a Free Fintech ConsultationThe Decision That Actually Determines Your Budget: Build vs. Integrate

Most fintech cost guides walk through features and stop there. That misses the decision that determines 30 to 50% of your total budget before a single feature gets scoped: how much of your financial infrastructure are you building versus integrating.

Austin’s own fintech story makes this concrete. Q2 Holdings, a publicly traded, Austin-headquartered digital banking provider with $795 million in annual revenue, doesn’t sell banks a finished app. It sells composable infrastructure, a marketplace of pre-integrated fintech capabilities that banks and credit unions plug into rather than build themselves. In 2026, Austin’s own A+ Federal Credit Union used exactly this model, implementing an end-to-end platform to consolidate its loan origination process instead of building it in-house, and reported a 202% increase in digital account openings and a 74.8% digital adoption rate among members as a result.

That’s not just a case study. It’s a signal about how fintech is actually getting built in Austin right now, and it applies just as much to a startup as it does to a credit union. It’s the same build-vs-integrate logic that shapes modern BaaS-powered fintech super apps like MoneyLion, where the winning products stack their own financial logic on top of licensed infrastructure rather than owning every layer themselves.

What this means for your build decision:

- Core banking, payments processing, and KYC/AML verification almost never need to be built from scratch. Providers like Plaid, Stripe, Unit, and Marqeta have already solved the compliance and infrastructure problem, and building your own version burns budget on solved problems instead of your actual differentiation.

- Your user experience, financial logic, and the specific workflow that makes your product different are where custom development earns its cost. This is where founders should be spending the budget that a build-everything approach would otherwise burn on undifferentiated infrastructure.

- The middle ground, where most real budget mistakes happen, is deciding late. Founders who scope integrations after starting custom development on features a BaaS provider already solves end up paying twice: once for the custom build, once for the rework when they realize the integration path was faster and more compliant from the start.

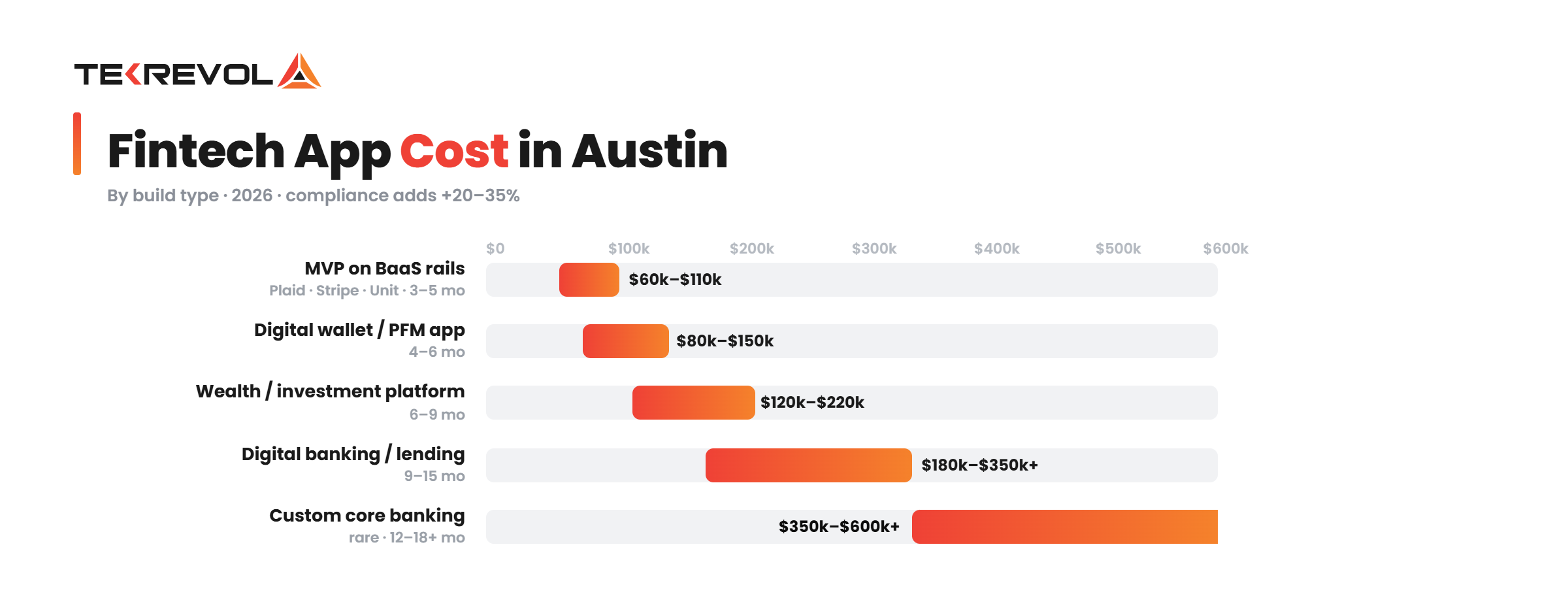

What Fintech App Development Actually Costs in Austin

| App Type | Cost Range | Timeline |

| MVP built on BaaS/compliance infrastructure (Plaid, Stripe, Unit) | $60,000–$110,000 | 3–5 months |

| Digital wallet or personal finance app | $80,000–$150,000 | 4–6 months |

| Wealth management or investment platform | $120,000–$220,000 | 6–9 months |

| Digital banking or lending platform | $180,000–$350,000+ | 9–15 months |

| Custom core banking infrastructure (rare, high-regulation) | $350,000–$600,000+ | 12–18+ months |

Compliance overhead adds 20 to 35% to the base development cost across every tier above. This covers PCI-DSS compliance for any app touching card data, SOC 2 Type II audit preparation for enterprise and B2B fintech products, and KYC/AML verification workflows for anything handling identity or money movement.

If you’re scoping the leanest possible version of any tier above, it’s worth understanding what an MVP actually needs to include, and what it can safely leave out, before you lock in a budget.

Not sure which tier fits your product?

Get a fintech app development quote scoped to your actual compliance and integration needs, not a generic template.

Book a Free ConsultationThe Compliance Requirements That Actually Drive Cost

Fintech compliance isn’t one requirement. It’s a stack of them, and which ones apply depends entirely on what your app does with money and data.

PCI-DSS compliance applies to any app that stores, processes, or transmits card data. Most fintech apps avoid building this themselves by routing card handling through a PCI-compliant processor like Stripe, which is the single biggest cost-saving integration decision most fintech founders make. This is the same compliance-first approach TekRevol lays out when building a fintech app like Klover, where PCI-DSS, GDPR, and Open Banking standards get built into the architecture from day one rather than bolted on before launch.

KYC (Know Your Customer) and AML (Anti-Money Laundering) verification is required for any app that opens accounts, moves money, or handles identity verification. Building this from scratch means integrating with identity verification providers, screening against sanctions lists, and maintaining audit trails, all before you’ve built a single user-facing feature.

SOC 2 Type II matters most for B2B fintech products selling into banks, credit unions, or enterprise finance teams, since it’s frequently a hard requirement in procurement, not a nice-to-have. The audit process itself typically takes 6 to 12 months of evidence collection before certification, so this needs to start early in the build, not after launch.

State money transmitter licensing applies if your app moves money on behalf of users in a way that goes beyond simple payment processing. This is a legal and regulatory question as much as a technical one, and it needs a compliance attorney involved before architecture decisions get locked in, not after. Lending-adjacent products, like BNPL apps, carry an even heavier version of this burden, since they’re typically classified as lending products and inherit CFPB oversight and state-by-state licensing requirements on top of standard payment compliance.

Texas-specific consideration: Texas has no state income tax, which is a genuine, practical reason fintech founders and senior engineering talent are choosing Austin over coastal hubs, not just a talking point. It doesn’t reduce your federal compliance burden, but it does mean your Austin-based team and talent pool come at a real, measurable cost advantage over New York or San Francisco equivalents.

What Each Feature Costs

| Feature | Estimated Cost |

| Bank account linking (via Plaid or similar) | $8,000–$18,000 |

| KYC/identity verification flow | $10,000–$25,000 |

| In-app payments and money movement | $15,000–$35,000 |

| Fraud detection and transaction monitoring | $20,000–$45,000 |

| Budgeting or personal finance dashboard | $12,000–$30,000 |

| Investment or trading interface | $30,000–$70,000 |

| Digital wallet infrastructure | $25,000–$60,000 |

| Biometric authentication | $8,000–$15,000 |

Fraud detection consistently surprises founders on cost. It’s not a feature you build once. It’s an ongoing system that needs tuning against real transaction patterns after launch, which is why the range above is wide: a static rules engine costs far less than an adaptive, ML-driven fraud model, and most fintech products need to plan for eventually needing the latter even if they launch with the former. It’s one of several must-have fintech app features founders consistently under budget for in 2026.

Ongoing Costs: What Fintech Founders Underbudget

A fintech app’s compliance obligations don’t end at launch. They’re the largest recurring cost category most founders miss when budgeting past year one.

Compliance maintenance and audits run $15,000 to $50,000+ annually depending on scope, covering SOC 2 recertification, PCI-DSS revalidation, and ongoing KYC/AML process audits. This is not optional and not occasional.

Third-party infrastructure fees scale with transaction volume. Payment processors, identity verification providers, and banking-as-a-service platforms typically charge per-transaction or per-verification fees that grow directly with your user base, which is a cost structure worth modeling before you set pricing, not after.

Fraud monitoring and model tuning requires ongoing engineering attention as fraud patterns evolve. A fraud model that worked at launch degrades in effectiveness as bad actors adapt, and budgeting for quarterly tuning is realistic, not excessive.

Security audits and penetration testing should happen at minimum annually, more often for products handling significant transaction volume, and this is a distinct budget line from general app maintenance.

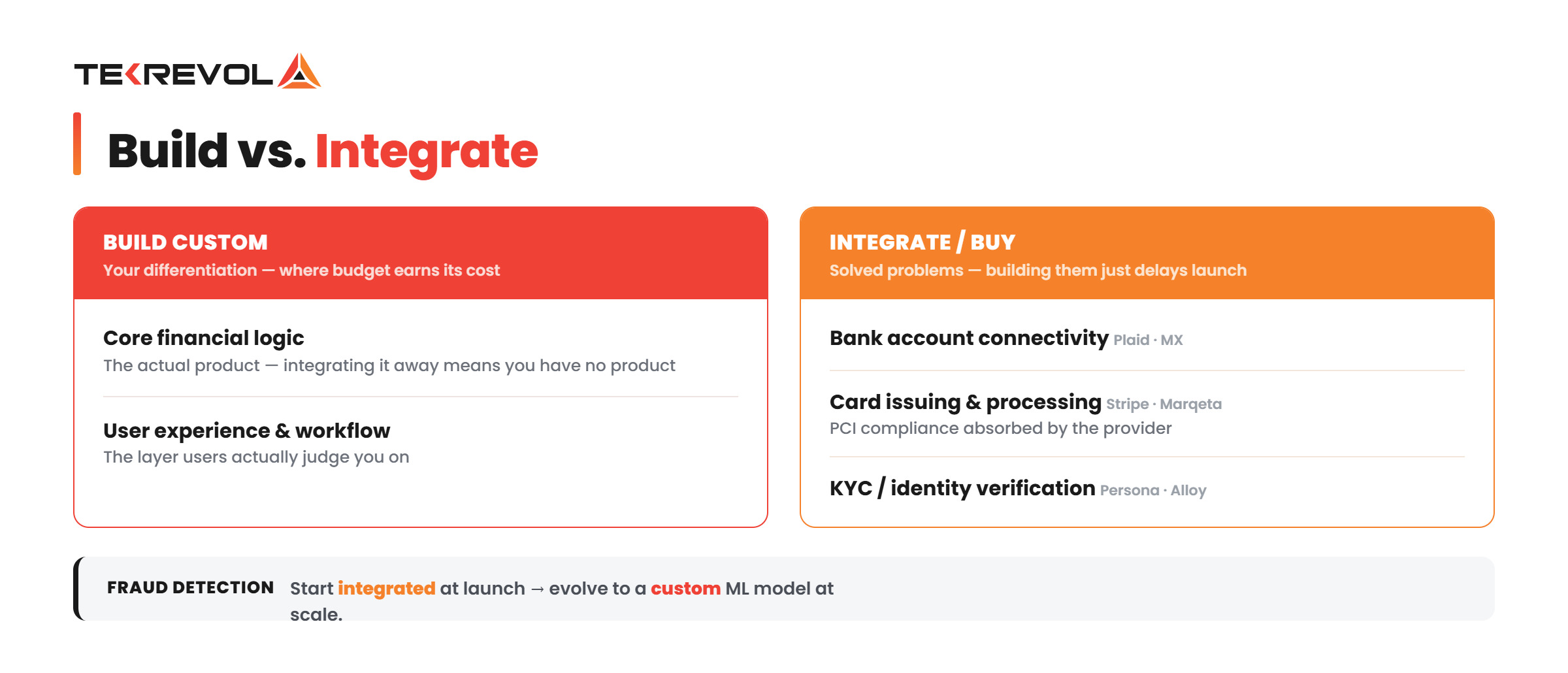

Build vs. Buy: A Practical Framework

Use this as a working framework for scoping your own build, not a universal rule; every fintech product has a specific reason to deviate from it.

| Component | Build Custom | Integrate/Buy | Why |

| Bank account connectivity | Rarely | Almost always (Plaid, MX) | Solved problem; building it delays launch for zero differentiation |

| Card issuing and processing | Rarely | Almost always (Stripe, Marqeta) | PCI compliance is absorbed by the provider |

| KYC/identity verification | Rarely | Almost always (Persona, Alloy) | Regulatory risk is too high to own alone at early stage |

| Core financial logic (your product’s actual value) | Almost always | Rarely | This is your differentiation; integrating it away means you don’t have a product |

| User experience and workflow | Almost always | Never | This is the layer users actually judge you on |

| Fraud detection rules | Start integrated, evolve custom | Initially | Off-the-shelf fraud tools work early; custom tuning matters at scale |

Curious how this compares to Austin app development costs outside fintech specifically?

TekRevol's Austin app development cost guide covers the broader cost factors like platform choice and team model that apply across every app category.

Start Your ProjectTwo Realistic Austin Fintech Build Scenarios

Scenario A: Embedded Finance Startup, Rent Reporting Platform

A seed-stage startup wants to build a rent payment and credit reporting product for renters and property managers, integrating with existing property management systems rather than building payment rails from scratch.

- Approach: Build on Plaid for account connectivity and Stripe for payment processing, focus custom development entirely on the credit-reporting logic and property management system integrations that constitute the actual product.

- Estimated cost: $95,000–$140,000 | Timeline: 5–6 months

Scenario B: B2B SaaS, Digital Banking Tools for Credit Unions

An Austin-based B2B fintech wants to sell workflow automation software to regional credit unions, following the same integration-first pattern that’s already proven locally.

- Approach: SOC 2 Type II certification process starts in parallel with development, not after. Core product logic is fully custom; underlying banking connectivity integrates with existing core banking platforms rather than replacing them.

- Estimated cost: $200,000–$280,000 | Timeline: 9–12 months, including the compliance certification runway

Questions to Ask Before You Hire a Fintech Development Partner

Fintech is one of the categories where the wrong technical decision doesn’t just cost money. It creates regulatory exposure.

- Have they actually shipped a compliant fintech product, or just a consumer app with a payments feature bolted on? These are different disciplines. Ask for a specific example, not a general claim of fintech experience.

- Do they understand the build-vs-integrate tradeoff, or do they default to building everything? A partner that proposes custom-building KYC or card processing from scratch, without discussing Plaid, Stripe, or comparable providers first, is either inexperienced in fintech or padding the scope.

- Who owns the compliance relationship, you or them? SOC 2 and PCI-DSS require an ongoing relationship with auditors and processors. A development partner should support this process, not disappear once the app ships.

- What’s their approach to fraud detection at launch versus at scale? A credible partner will tell you a static rules engine is fine at launch and a custom model comes later, not oversell an enterprise fraud system your MVP doesn’t need yet.

- Can they show a project in a similar budget range? TekRevol’s own financial services project work most commonly falls between $10,000 and $199,999, which is a useful benchmark for whether a proposed budget is realistic for your stage. As a mobile app development company in Austin, TekRevol scopes these engagements against the same local cost and compliance realities covered in this guide.

Building Fintech in Austin? Let’s Scope It the Way Austin’s Own Fintech Leaders Do

The founders getting fintech products to market fastest in Austin right now aren’t building everything themselves. They’re following the same pattern Q2 Holdings has proven at scale: build your actual differentiation, integrate everything else.

TekRevol’s fintech development work spans digital banking, wealth management, digital wallets, and payment platforms, with a security-first approach that treats PCI-DSS and KYC/AML compliance as architecture decisions from day one, not a checklist before launch.

Ready to scope your fintech build the smart way?

Talk to TekRevol's fintech app development specialists for an itemized estimate within 48 hours.

Book a Free Consultation