Ever sent an important email and thought, “I really hope this doesn’t get into the wrong hands”? Or shared data with a company and just trusted they’d keep it safe? Yeah, we’ve all been there. Now imagine if that trust wasn’t a leap of faith, but a built-in feature. That’s how blockchain works. And no, it’s not just a crypto thing anymore.

With an increase in data breaches and rising distrust of centralized systems, blockchain services are becoming a revolutionary force. What started as the backbone of cryptocurrencies is now leading to innovation in finance, logistics, and digital identity management. These blockchain applications are why businesses increasingly explore blockchain solutions.

Nearly 83% of the surveyed executives suggest that failing to include blockchain could make their organizations less competitive strategically. So, exactly how does blockchain work step by step in the first place? Let’s demystify.

What is Blockchain Technology? An Overview

Blockchain is a decentralized way of digital recordkeeping where computers store transactions on a network. In contrast to normal databases, which rely on a single authority, blockchain allows information to be shared among users, so no middleman is necessary for transparency, safety, or trust. What makes it so strong? Once information enters, it can’t be altered.

If you’ve ever wondered what is a blockchain in crypto, Bitcoin (2009) was the first blockchain example. Today, the technology supports:

- Cryptocurrencies such as Ether and Solana

- Decentralized finance (DeFi) platforms for lending, trading, and yield farming

- Non-fungible tokens (NFTs), which verify ownership of digital possessions

- Smart contracts are autonomous, programmatic agreements that execute functions on preset conditions

- Enterprise solutions for supply-chain tracking, healthcare record-keeping, digital identity, and more

- Unlock the Power of Blockchain for Your Business

- We help tech founders build secure, scalable, and future-ready blockchain solutions.

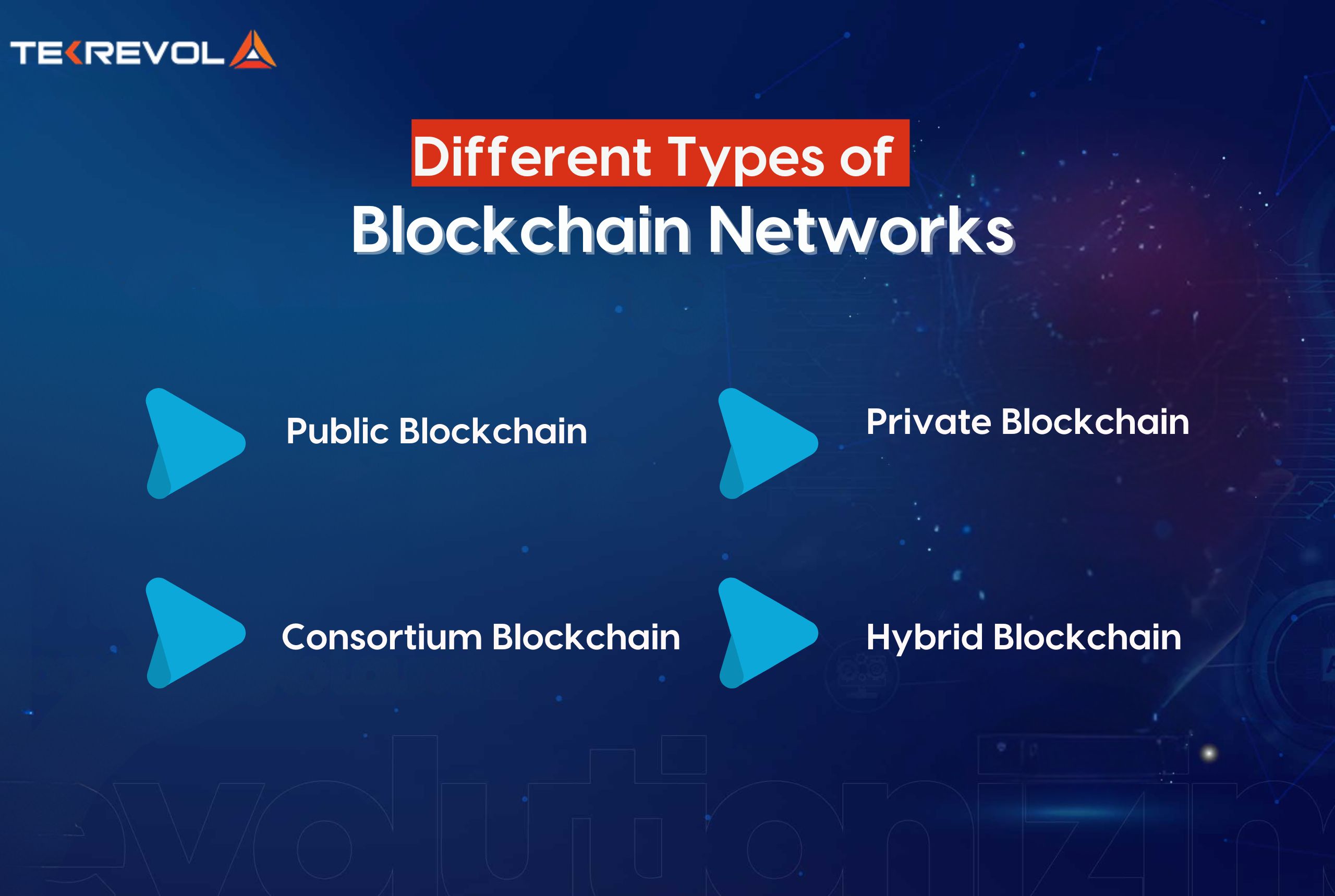

Different Types of Blockchain Networks

As you explore how blockchain works, it’s important to understand the different types of blockchain networks. Each type offers unique trade-offs in terms of transparency, decentralization, and control. Businesses and startups choose their model based on goals like scalability, privacy, and security.

1. Public Blockchain

A public blockchain is an open, permissionless network accessible to anyone. It is fully decentralized, without central control. Members can join without disclosing their identity, and security is ensured by consensus mechanisms such as Proof of Work (PoW) or Proof of Stake (PoS).

- Accessible worldwide

- No central authority

- Transactions validated via mining or staking

- Examples: Bitcoin, Ethereum (also widely used for DeFi, NFT applications, and decentralized apps)

2. Private Blockchain

Private blockchains restrict access to approved participants only. Governed by a single organization, they provide more control over permissions, making them ideal for enterprises or government agencies that need privacy and strict data governance.

- Access restricted to authorized users

- Centralized oversight by one organization

- Suited for confidential data and internal processes

- Often deployed for enterprise-grade blockchain services

3. Consortium Blockchain

Also known as federated blockchains, consortium blockchains are jointly governed by multiple organizations. This cooperative structure enhances efficiency while maintaining trust, and it’s especially popular in finance and supply chain management.

- Shared control among a predetermined group

- Collaborative validation of transactions

- Combines decentralization with structured governance

- Common in banking, logistics, and healthcare industries

4. Hybrid Blockchain

Hybrid blockchains combine the strengths of public and private networks. They allow organizations to keep certain data private while making other information publicly verifiable — perfect for industries balancing transparency and confidentiality.

- Mix of public transparency and private security

- Customizable access controls

- Protects sensitive information while enabling auditability

- Useful in metaverse platforms and regulated sectors like healthcare

Foundational Elements of Blockchain Technology

As we dive deeper into how blockchain works, it’s clear that its power goes beyond cryptocurrencies. These foundational elements are the building blocks behind innovations like NFT development, DeFi apps, and even metaverse development platforms. From fundraising models to digital ownership, here are the pillars shaping blockchain in 2025.

1. Token-Based Fundraising: The Role of ICOs

Initial Coin Offerings (ICOs) once served as a major fundraising vehicle for blockchain startups. While still relevant, many have been replaced or complemented by newer models like STOs (Security Token Offerings) and IEOs (Initial Exchange Offerings).

Phases of an ICO:

- Preparation & Whitepaper Drafting: Startups prepare a detailed roadmap, tokenomics, and project vision.

- Public Disclosure & Token Info: Details about allocation, pricing, and utility are shared with potential investors.

- Token Allocation: Digital tokens are exchanged for cryptocurrency like ETH or BTC to fund development.

- Marketing Initiatives: Campaigns run across social channels, crypto forums, and online events to build momentum.

2. Smart Contracts: Empowering Self-Executing Agreements

Smart contracts are self-executing agreements coded on the blockchain. Unlike traditional contracts requiring intermediaries, these agreements enforce themselves when predetermined conditions are met.

Why Smart Contracts Matter:

- Trustless execution — governed directly by the blockchain

- Escrow-like protection — funds released only when rules are met

- Faster processes — reducing paperwork and human error

- Applied across industries: real estate, insurance, supply chains, finance

Smart contracts form the backbone of decentralized apps (dApps), blockchain services, and next-gen metaverse ecosystems.

3. Crypto Wallets: The Portal to Blockchain Interaction

To truly grasp how blockchain works for beginners, you must understand Cryptocurrency wallets. They’re the interface between users and the blockchain. Wallets store private keys and allow sending, receiving, and managing digital assets.

Types of Wallets:

- Hot Wallets: Always online for easy access (e.g., mobile apps, browser extensions).

- Cold Wallets: Offline wallets that provide additional security (e.g., hardware wallets, paper wallets).

- Software Wallets: PC or mobile-based wallets designed for simplicity.

- Web Wallets: Accessible through browsers and hosted online, which provides convenience to casual users.

Wallets are essential for managing cryptocurrencies, accessing dApps, and engaging in NFT marketplaces.

4. NFTs: Defining Digital Ownership

NFTs (non-fungible tokens) represent verifiable ownership of unique digital assets such as art, music, videos, or even land in virtual worlds.

Key Features of NFTs

- Uniqueness: Each NFT has an identity and metadata that make it irreplaceable.

- Ownership & Authenticity: Clear ownership and provenance through blockchain.

- Smart Contract Backing: Most NFTs have smart contracts supporting the movement of royalties and ownership.

Ethereum dominates the NFT development process, though alternatives like Solana, Polygon, and Binance Smart Chain are becoming popular due to lower costs and faster speeds. NFTs are not only fueling art and collectibles but also driving innovation.

How Does Blockchain Work? A Step-by-Step Breakdown

At its core, blockchain is a digital ledger, but unlike traditional databases, it is decentralized, transparent, and highly secure. To truly understand how blockchain works step by step, let’s break down its essential mechanics.

Blocks: Where the Data Reside

Each item of data on a blockchain resides in a “block.” Each block contains:

- The actual information (such as a record of a transaction),

- A special code called a hash (imagine it as a digital fingerprint),

- And the previous block’s hash.

These hashes are made using advanced cryptography techniques. If someone tries to tamper with a block, a different hash is automatically generated, cutting the connection to the following block and informing the network there is a problem. Because of this process, blockchains are not easy to change and are highly secure.

Decentralization: No Middlemen Needed

Instead of a single central server, blockchain relies on a peer-to-peer network of nodes. They verify it using consensus mechanisms like PoW (Proof of Work) or PoS (Proof of Stake). Only after consensus is achieved is a new block added. This is how blockchain works for beginners: a community-driven system with no single point of control, enhancing transparency and trust.

Smart Contracts: Automating Trust

Beyond simple transactions, blockchain can run smart contracts (self-executing agreements coded into the chain). These enable automation across industries, from real estate to supply chains, and power innovations in metaverse ecosystems.

Immutability: Write Once, Never Erase

Once data is added, it becomes part of a permanent record. Transactions are transparent, auditable, and tamper-resistant. This makes blockchain ideal for applications requiring traceability, like logistics, compliance, and digital identity.

Top Benefits of Using Blockchain

Understanding how blockchain works also means recognizing the advantages it brings across industries. From fintech software development services to metaverse platforms, blockchain is revolutionizing how organizations operate. Here are the major benefits:

Increased Security

- Leverages cryptographic techniques to encrypt and chain each transaction to the last.

- Consensus algorithms such as Proof of Work (PoW) or Proof of Stake (PoS) confirm each block.

- Decentralized architecture eliminates points of failure, decreasing exposure to hacks and fraud.

- Information, once written, is resistant to tampering and fixed.

Increased Accuracy & Transparency

- Network verifies and timestamps all transactions before adding them to the ledger.

- Data is made visible to all participants, providing one unified, open source of truth.

- Eliminates risks of human error, misreporting, or unapproved data changes.

- Prohibits full traceability and auditability of records.

Greater Efficiency & Automation

- Eliminates intermediaries through peer-to-peer interaction.

- Smart contracts streamline workflows, reducing paperwork.

- Cuts operational costs across departments.

- Speeds up processes in areas like blockchain services and supply chain management.

Improved Traceability

- Ideal for tracking supply chain and logistics.

- Provides real-time visibility into product origin, location, and movement.

- Assists with authenticity verification (e.g., luxury items, pharmaceuticals).

Cost Reduction

- Eliminates transaction fees and administrative costs.

- Reduces the requirement for third-party services such as auditors, escrow agents, etc.

- Avoids fraud and related financial losses.

Decentralized Control

- Empowers individuals by eliminating dependence on a central authority.

- Increases trust among stakeholders in public and private sectors alike.

- Well-suited for democratic governance models or open networks.

- Ready to Integrate Blockchain into Your Startup?

- We offer strategy, development, and launch support for blockchain-powered platforms.

Ongoing Challenges in Blockchain Technology

While we’ve seen how blockchain works and its many benefits, the technology still faces major hurdles that slow mainstream adoption. These challenges impact industries from finance to metaverse development and NFT development.

Limited Scalability

- Every node verifies transactions and keeps a full ledger copy.

- Network congestion causes slower speeds and higher fees.

- Layer 2 solutions, sharding, and new consensus mechanisms aim to solve this.

High Energy Consumption

Consensus mechanisms such as Proof of Work, particularly in networks such as Bitcoin, require enormous computing power, resulting in exorbitant electricity consumption and environmental issues.

The transition to energy-efficient options such as Proof of Stake is already happening, but bulk adoption will require time.

Transaction Speed and Capacity Issues

- Legacy frameworks can’t always support high-frequency use cases (e.g., payments, gaming, DeFi).

- Bottlenecks lead to higher costs and delays during peak traffic.

- Emerging blockchain architectures are tackling throughput with mixed success.

Changing Regulatory Environment

- Blockchain’s decentralized nature makes regulation complex.

- Governments worldwide are drafting new policies, but clarity is lacking.

- Businesses struggle to balance compliance, security, and innovation.

- A clear regulatory framework is vital for blockchain developers and investors to scale safely.

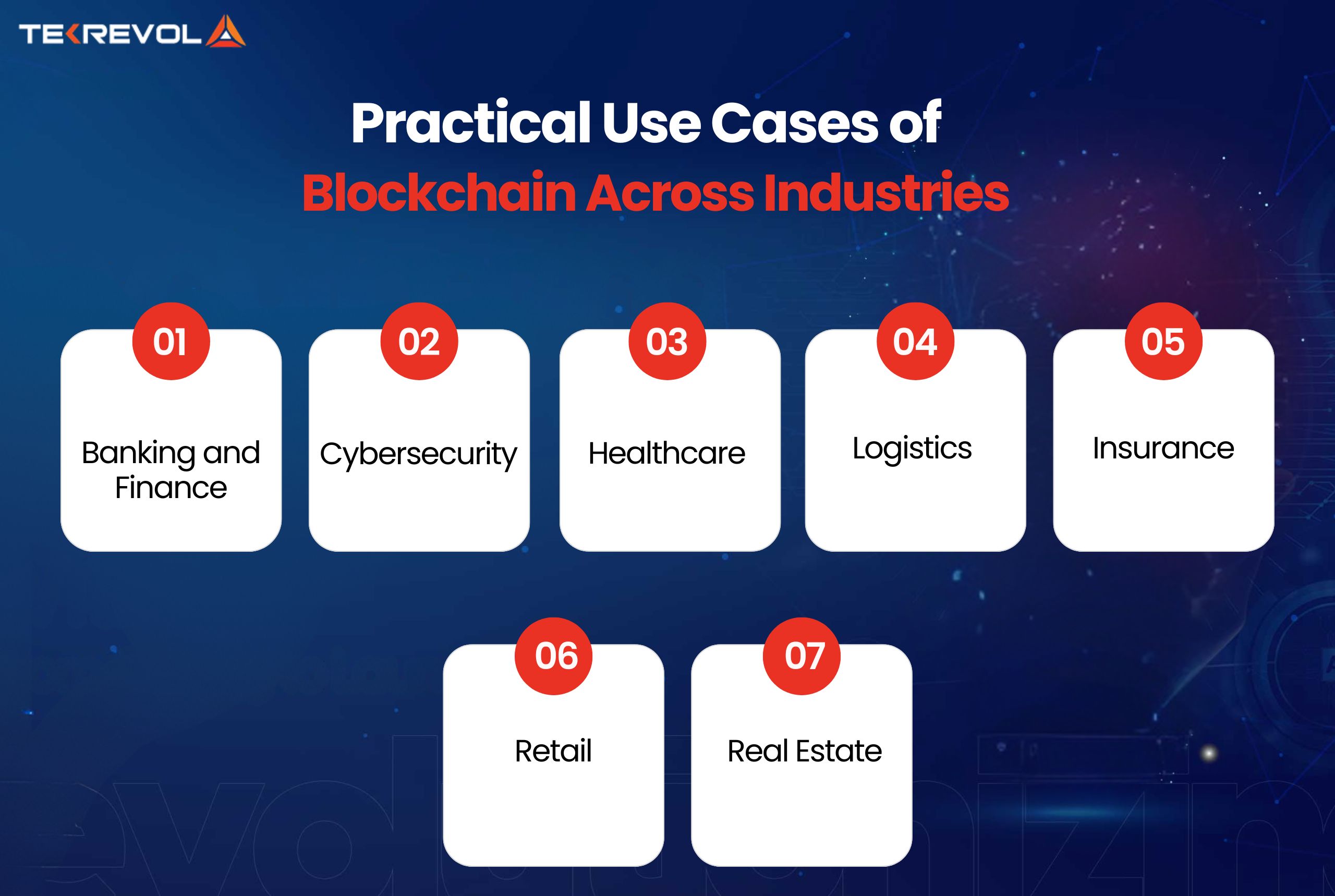

Practical Use Cases of Blockchain Across Industries

Now that you’ve explored how blockchain works, let’s look at how the technology is reshaping industries with real-world applications. From finance to retail, blockchain provides transparency, efficiency, and trust in processes that once relied heavily on intermediaries, making it an essential consideration for any mobile app development strategy integrating blockchain solutions.

Banking and Finance

Blockchain offers banks a transparent and secure financial transaction management system. It lowers the risk of fraud, accelerates payments, and saves costs.

- Immutable records of transactions: All transactions are recorded and authenticated immutably, reducing fraud.

- Quicker settlements: Cross-border and local payments settle much faster than conventional systems.

- Less expensive: Less reliance on intermediaries reduces fees on transactions.

- Anti-money laundering: Inherent tracing assists in the detection of suspicious activity in real time.

- Encryption of data: Confidential financial information is safeguarded by cryptographic techniques.

Cybersecurity

Blockchain provides an enhanced layer of security against hacking and unauthorized use.

- Decentralized storage: Data is distributed between several nodes, avoiding single points of failure.

- Cryptographic security: Data is encrypted and attached to earlier blocks for resistance to tampering.

- Access control: Authorized users are the only ones able to decrypt sensitive information.

- Fraud prevention: Consensus algorithms check for legitimacy before storing.

- Wide usage: Utilized to protect anything from cryptocurrencies to defense and healthcare information.

Healthcare

Blockchain protects patient information and automates processes, making innovations like healthcare app development more secure and trustworthy.

- Data encryption: Securely stores and protects patient records.

- Interoperability: Enabling safe sharing of data among hospitals, labs, and researchers.

- Smart contract automation: Accelerates insurance claims and patient monitoring workflows.

- Less admin: Reduces paperwork and manual authentication steps.

Logistics

Blockchain increases supply chain management through real-time tracking and transparency.

- End-to-end visibility: Monitor products from production to delivery.

- Data integrity: Tamper-proof and fraud-proof records.

- Optimized routes: Insights minimize delays and save costs.

- Fewer intermediaries: There are fewer middlemen, and operations are streamlined.

- Cybersecurity: Shields the supply chain from cyberattacks.

Insurance

Blockchain revolutionizes insurance by providing clearer claim processing and higher efficiency.

- Real-time claim tracking: All the claims are stored and viewed on an impenetrable ledger.

- Fraud reduction: Avoids duplicate and false claims.

- Process automation: Smart contract accelerates quick approvals and payments.

- Less paperwork: Automated processing is time and cost-efficient

- Greater customer trust: Open claims handling fosters trust.

Retail

Merchants employ blockchain to enhance product openness and consumer confidence.

- Product traceability: Connect physical products with digital accounts using QR codes or IoT sensors.

- Ethical sourcing: Track and present responsible manufacturing practices.

- Inventory management: Real-time tracking minimizes stock differences.

- Customer engagement: Present buyers with an authentic product history.

- Supply chain security: Guard against fake products and fraud.

Real Estate

Blockchain facilitates real estate transactions and property management through secure record-keeping.

- Ownership records: Secure property titles and transaction histories.

- Tenant verification: Background and credit checks are automated.

- Paperwork efficiency: Lease, ID, and insurance documents are digitally stored.

- Compliance enforcement: Smart contracts enforce regulatory compliance

- Faster closings: Efficient processes eliminate delay.

How Secure Is Blockchain Technology?

When people first learn how blockchain works, one of the biggest questions that comes up is: just how secure is it? The answer lies in the core principles of decentralization, immutability, and cryptography that make tampering nearly impossible.

At its foundation, each block in the chain contains:

- A cryptographic hash of the previous block

- A timestamp

- The transaction data

This structure means that to alter any single record, one would need to modify every subsequent block across the majority of nodes — something computationally unfeasible.

Important Features That Fortify Blockchain Security

- Decentralization: Eliminates a single point of failure, as data is distributed across nodes.

- Cryptography: Advanced algorithms encrypt data so only authorized participants can access it.

- Consensus Mechanisms: Protocols like Proof of Work (PoW) and Proof of Stake (PoS) validate transactions and prevent double-spending.

- Immutability: Once data is added to the chain, it cannot be erased or altered without network-wide agreement.

- Transparency with Anonymity: Transactions are visible and verifiable, yet user identities remain protected through pseudonymous addresses.

Thanks to these safeguards, businesses exploring blockchain services and solutions can trust the system to provide security while maintaining openness. Whether you’re a blockchain developer building new platforms or a company testing pilots, the reliability of this architecture is one of the key reasons adoption continues to grow.

Note: Since you’re now familiar with blockchain technology and how it functions, and you’d like to proceed to create your own blockchain application, take a look at our detailed guide: “How to Develop Blockchain Applications: The Ultimate Roadmap for Businesses.”

Wrapping Up

Understanding how blockchain works step by step makes it clear why this technology is reshaping industries worldwide. From banking and healthcare to logistics and real estate, blockchain applications deliver transparency and efficiency that traditional systems can’t match.

Now, tailored blockchain solutions and professional blockchain services are no longer optional but a strategic necessity. Whether safeguarding sensitive data or building decentralized platforms, the right blockchain developer can turn innovation into impact.

Even for those learning how blockchain works for beginners, the opportunity is significant. Startups and enterprises alike can leverage blockchain to reduce costs and future-proof operations. If searching for a reliable partner, TekRevol is a blockchain app development company. Our expertise in blockchain strategy and development can help you lead in the digital economy.

- Take the next step in your digital evolution.

- Let TekRevol help you lead the change with powerful blockchain app development.